Multinational enterprise groups tend to centralise their functions, such as support functions in a region that is economically important and advantageous. Particularly interesting cases of transfer pricing (TP) determinations and valuations involve a group’s distributors (intermediaries) that make centralised purchases of goods from the group manufacturers and sell them on to the group wholesalers. This article looks at TP challenges in such economically linked transactions within the same global supply chain.

A multinational enterprise group operates in the consumer goods sector. Given the global operations of the group companies, there were sound economic reasons for making a strategic decision to reorganise the group structure, centralise the distribution function and therefore set up central purchase and distribution companies in the key markets the group operates in.

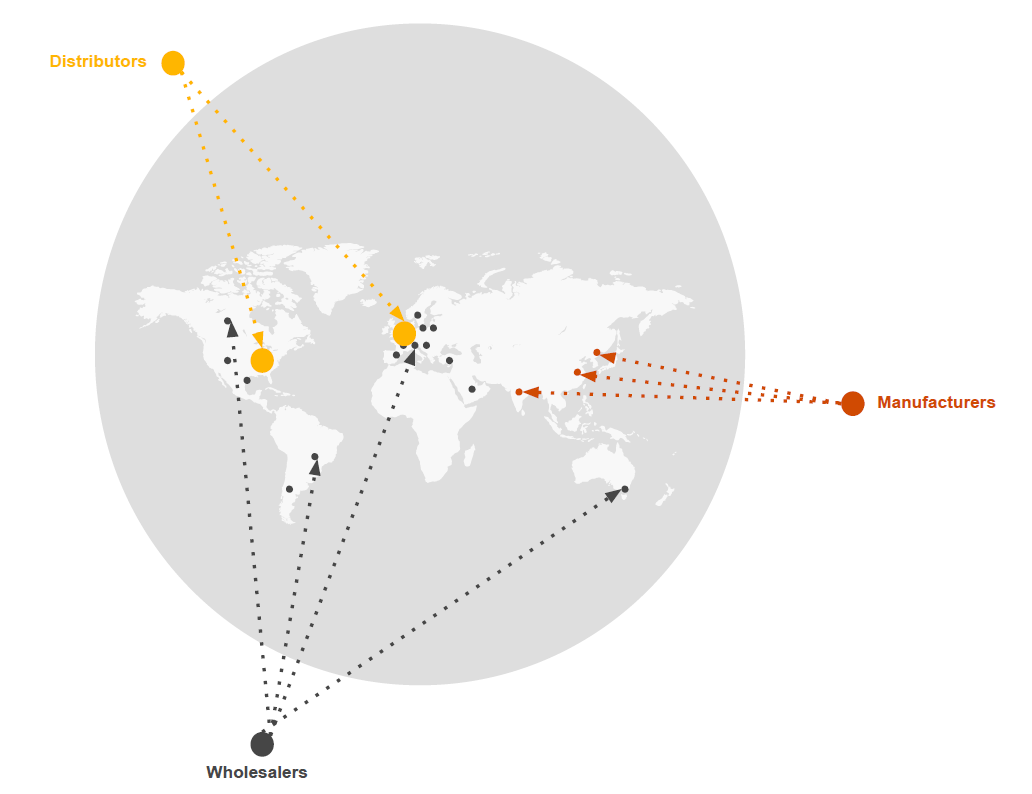

The figure below shows the group’s worldwide operations:

Centralising the distribution function helps to ease the manufacturers’ administrative burden that arises from collecting and fulfilling large orders from the wholesalers. Given their geographical markets, the wholesalers place orders with the distributor representing the relevant market, rather than with each of the manufacturers.

The distributors collect all the orders they receive from the wholesalers for their relevant markets and pass them on to the manufacturers as a single order. To ease the burden of making transport arrangements, this function is also centralised and performed by the distributors.

Given its structure and related-party transactions, the group needs to demonstrate that the price of its controlled transactions is arm’s length.

The distributors face the biggest TP challenge if their purchases and resales are large and only with related parties. In other words, the cost of goods sold arises only in controlled purchases and there are no uncontrolled sales. In this case it is not possible to credibly compare their prices with an arm’s length price. It’s also difficult to identify an appropriate financial indicator that could be properly used for checking that it’s arm’s length if the tested party whose financial indicators are to be analysed is the distributor with no access to segmented financial data of the wholesalers and manufacturers.

According to TP practice, to show that the selected financial indicator arising in a related-party transaction is arm’s length, the denominator of the formula for computing the indicator must be revenue or cost that is not controlled. In our case, however, when we compute the distributor’s margin or markup, both revenue and cost are controlled. So we need to find another indicator reflecting a credible result of the distributor’s business.

To approximate the circumstances of unrelated parties, the OECD TP guidelines recommend that other financial indicators being used in TP analysis may be appropriate depending on the facts and circumstances of each case.

Chapter B.3.5 of the OECD TP guidelines (the January 2022 version) offers information on the Berry ratio. According to paragraph 2.108 the Berry ratio may be used for intermediary activities when a taxpayer buys goods from a related company and sells them on to another related company.

The Berry ratio compares a company’s gross profit to its operating expenses. Interest and extraneous income are generally excluded from the gross profit determination. Depreciation and amortisation may or may not be included in the operating expenses, depending in particular on possible uncertainties they can create around valuation and comparability.

In view of this, the distributor can use the Berry ratio for determining and evaluating his TP in order to check his remuneration for controlled transactions. However, before the distributor can use the Berry ratio for a remuneration check, there are certain requirements and conditions he has to meet, i.e. he needs to undertake a financial data segmentation. He should also be aware that the availability of comparable financial data will be limited. In our next article we’ll be exploring those requirements and conditions.

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question