Our experience suggests that the State Revenue Service (SRS) has recently focused on checking how Latvian corporate taxpayers fulfil their obligation under transfer pricing (TP) legislation,i.e. (1) whether they have prepared TP documentation in the prescribed form by the statutory deadline and (2) whether their documentation gives all the required information to verify that their controlled transactions are arm’s length.

The SRS will first check to see if the taxpayer has met his obligation for the last period in which TP documentation had to be prepared and filed (i.e. FY20). However, section 23(1.1) of the Taxes and Duties Act authorises the SRS to assess and adjust the taxpayer’s taxable income (loss) and charge a penalty during a TP audit within five years after the statutory tax payment deadline.

This rule has many clients wondering how to calculate the last five years that are open to a TP audit and how to determine the last year the taxpayer should not forget about.

To work out the last year for which the SRS may adjust your TP, you need to consider the payment deadline for the corporate income tax (CIT) charged according to your final CIT return for the year under the CIT Act.

It’s also important to be aware that the CIT Act effective from 1 January 2018 changed the deadline for paying the tax charge stated on the CIT return. It was brought forward from the 15th day of the fifth month of the following financial period to the 23rd day of the first month of the following financial period.

Let us look at an example of how to determine the years open to TP adjustment.

Suppose a taxpayer’s financial year coincides with the calendar year. At the time of writing this article, the taxpayer had filed his last CIT return for 2021 by 20 January 2022 and paid the tax charge by 23 January 2022. We start off by counting five years back from this tax payment period:

The picture allows us to conclude that the SRS may conduct a TP audit and decide on the audit result (TP adjustment) for transactions made in 2017.

As we have written before, since 2013 the taxpayer has been allowed to apply to the SRS for entering into an advance pricing agreement (APA).

The taxpayer may benefit from an APA in a number of ways. What matters is that during the operation of the APA, the SRS has no right to adjust the agreed arm’s length price for a particular transaction or type of transaction during an audit or any other tax control if the taxpayer has complied with the APA and no change has been made to his business in breach of the APA.

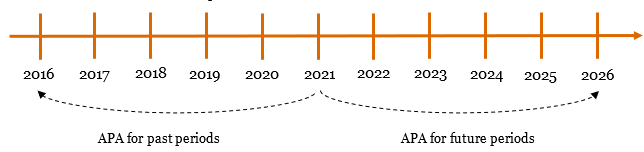

Although an APA is traditionally concluded for the next five financial periods, amendments to section 16.1(11) of the Taxes and Duties Act effective from 1 January 2019 permit the APA procedure to be initiated also for past financial years unless the statutory five-year period of limitation for a TP audit has expired:

If his controlled transactions are material, the taxpayer should consider entering into an APA with the SRS.

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question