With the financial year nearing its end, section 15.2 of the Taxes and Duties Act requires many companies to prepare, or to prepare and file with the State Revenue Service (SRS), their transfer pricing (TP) documentation. Since determining related-party status often confuses taxpayers and authorities, this article reminds you who is considered a related party for TP purposes and what transactions require the taxpayer to prepare TP documentation.

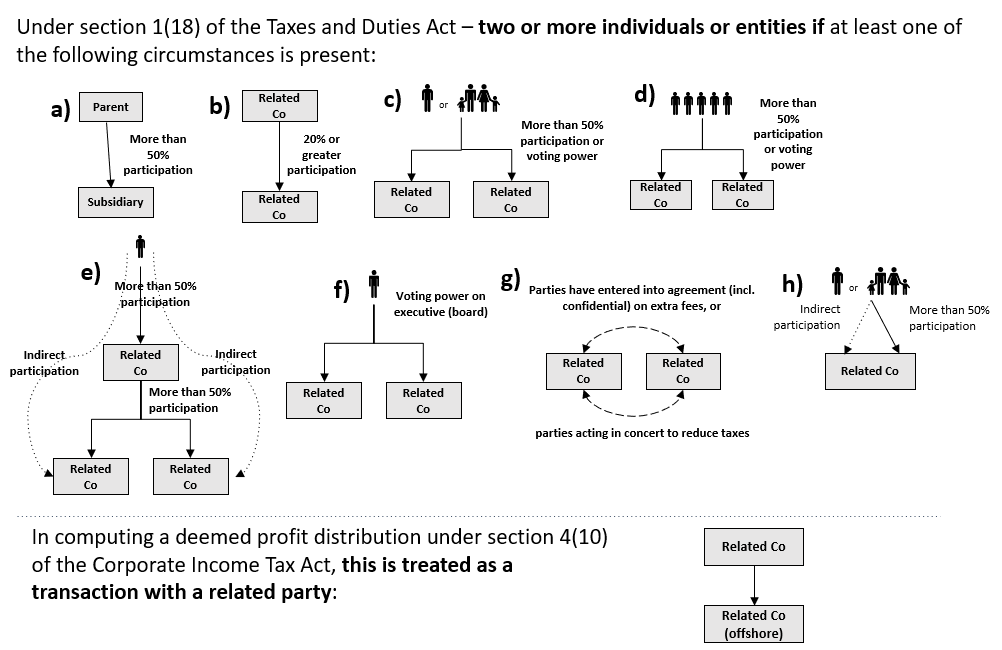

Related parties for TP purposes are defined by section 1(18) of the Taxes and Duties Act, which in general consists of eight paragraphs. Section 4(10) of the Corporate Income Tax Act additionally refers to a transaction that for TP purposes is considered a transaction with a related party. The picture below summarises those nine paragraphs:

Under section 15.2(2) of the Taxes and Duties Act, a resident taxpayer or a permanent establishment has to show the arm’s length nature of controlled transactions it makes with:

The easiest way to acquire related-party status is by meeting the condition of direct participation, i.e. one company owns 20% or more shares in another. If it is not possible to identify a relationship through the entity, we need to assess whether the companies are related through an individual, a family or a group of up to ten individuals, i.e. the individual, family or group directly or indirectly holds more than 50% of shares in several companies. After assessing these and more complex situations shown in the picture, companies acquire related-party status and have to prepare and/or file TP documentation under TP rules.

For transactions with a tax-haven entity/person, it does not matter whether the company with which the transaction is made is a related party, i.e. any transaction with a company located in any of the countries or territories listed in the Cabinet of Ministers’ Rule No. 819, Offshore Tax Havens, must be described in the TP documentation. However, the number of blacklisted jurisdictions has significantly dropped in recent years, leaving only nine, so in practice such transactions are becoming increasingly rare.

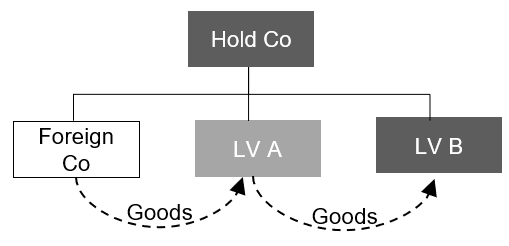

An obligation to validate TP also arises in transactions between residents if a transaction occurs within a chain of supplies involving a related foreign company or a tax-haven entity/person. For example, if Latvian company A buys goods from a related foreign company and sells them on to related Latvian company B (see picture below), the transaction between A and B must be analysed in the TP documentation.

For transactions between residents within a chain of supplies, the taxpayer is not required to prepare a specified form of TP documentation beforehand. Under section 15.2(7) of the Taxes and Duties Act, this obligation only arises at the SRS’s request. The taxpayer is allowed 90 days after receiving a request to prepare and file with the SRS a specified form of TP documentation, and this time limit can be extended for 30 days.

While there is no requirement that transactions between Latvian residents should be documented for TP purposes (as can be seen from the above), remember the SRS can also check to see if such transactions are arm’s length. In this case the taxpayer is not required to prepare a specified form of TP documentation but is required to show the transactions are in line with basic TP principles at the SRS’s request. So it would be good practice to regularly verify the arm’s length nature of resident transactions as well, by preparing a separate TP analysis that can be used later in preparing the TP documentation requested by the SRS.

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question