The European Central Bank (ECB) has been increasing its key interest rates since June 2022 to mitigate the high inflation caused by Covid-19. Taxpayers have good reason to debate whether they should revise the interest rates historically applied in their long-term financing transactions between related parties and apply new rates that are arm’s length and reflect the current economic conditions. This article explores the vision of the State Revenue Service (SRS) and recommendations for mitigating potential transfer pricing (TP) risks.

The low interest rate environment prevailing over the last 15 years had partially reduced taxpayers’ awareness of TP risks associated with financing transactions. This became an issue when EURIBOR rates began to rise. We often see low rates charged on loans between related parties, yet the ECB policy has raised the question of whether those interest rates are appropriate for the actual market conditions and there is the risk of historical interest rates no longer being arm’s length.

During a TP seminar held by the SRS at the Latvian Chamber of Commerce and Industry in May 2021, an SRS official expressed the opinion that TP in loan transactions between related companies should not be revised during the operation of their agreement unless the agreement provides otherwise.

However, in the light of the basic TP principles, we should consider the significant changes to the market conditions and wonder whether unrelated parties to a comparable transaction would be willing to continue doing business on the historical terms once the market conditions have changed. There is good reason to believe that unrelated parties would be willing to revise the interest rate, in particular if the agreement is for a long period.

So, if the related parties decide not to revise their interest rate, there is the risk that during a tax audit the SRS will find that the transaction is not arm’s length.

Given the SRS’s opinion and TP experience, we recommend that companies wishing to mitigate TP risks and take preventive steps should revise their interest rate according to the current market conditions.

For this purpose the taxpayer should undertake a similar analysis to the one conducted before the loan transaction and evaluate the latest comparables published by the Bank of Latvia (BOL). This will help the taxpayer understand whether its current interest rate is arm’s length or whether it should be increased or reduced.

To understand what this revision could look like in practice, let’s look at a theoretical example.

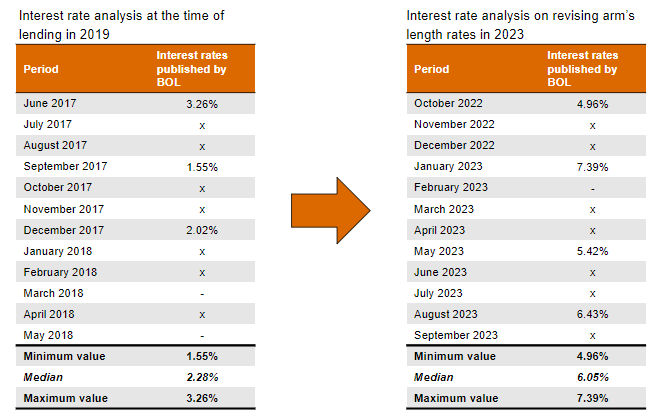

In July 2018 a Latvian taxpayer entered into a EUR 5 million long-term loan agreement with a related foreign company. The loan matures in seven years, and the original interest rate in the agreement was set according to weighted average interest rates published by the BOL.

Because the BOL publishes statistics with a two-month delay, the taxpayer selected data for the 12-month period running from June 2017 to May 2018 and determined an arm’s length range at the time of lending. The taxpayer selected an arm’s length rate of 2.20%, which is close to the median (see the original arm’s length range in the picture below).

Given the changing market conditions, in November 2023 the taxpayer decided to take preventive steps and revise the interest rate in the light of the market conditions. As before, the taxpayer used weighted average interest rates published by the BOL for the 12-month period running from October 2022 to September 2023 and determined a new arm’s length range:

As you can see in this theoretical example, the original interest rate of 2.20% is not consistent with the market conditions and high interest rates prevailing in 2023. After this analysis, the taxpayer revised the original interest rate and set a new rate of 5.10%.

We can conclude that if a loan were made on the same 2018 terms in August 2023, an arm’s length interest rate would range from 4.96% to 7.39%.

Given the materiality of the transaction, this interest rate differential would make a fairly big impact on the taxpayer’s corporate income tax base, increasing the risk of the SRS challenging the interest rate and making a TP adjustment.

Given the changing market conditions, we recommend that taxpayers involved in financing transactions with related parties should revise the interest rates applied on those transactions. In particular, this applies to fixed-rate long-term transactions made up to June 2022, when the ECB began to raise its key interest rates. This analysis can be based on statistics published by the BOL and the ECB, which can be accessed free of charge. Companies can also conduct this analysis using their credit rating analysis access to paid databases.

Taxpayers are advised to include the new terms in amendments to their agreement. This will substantially mitigate risks and make it easier to communicate with the SRS on a tax audit.

As you may know, transfer pricing is not an exact science, to quote the OECD TP guidelines.1 Both the tax authority and the taxpayer should reasonably evaluate the facts and circumstances of each financing transaction.

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question