We have written before about the profit split method (PSM) and its potential in transfer pricing (TP) analysis, looking at the essence of this method and the scope for using it. This article explores PSM’s advantages and disadvantages.

The available information on PSM tells us that TP analysis faces two kinds of situations. In some situations PSM would be useful and even desirable, while in other situations this method is overly complex and fails to produce a sufficiently reliable result for assessing a controlled transaction’s compliance with the arm’s length principle.

The value chains of multinational enterprises (MNEs) are becoming more and more complex, which makes it difficult to find appropriate comparables, so the traditional TP methods1 are unable to produce reliable results in such situations.

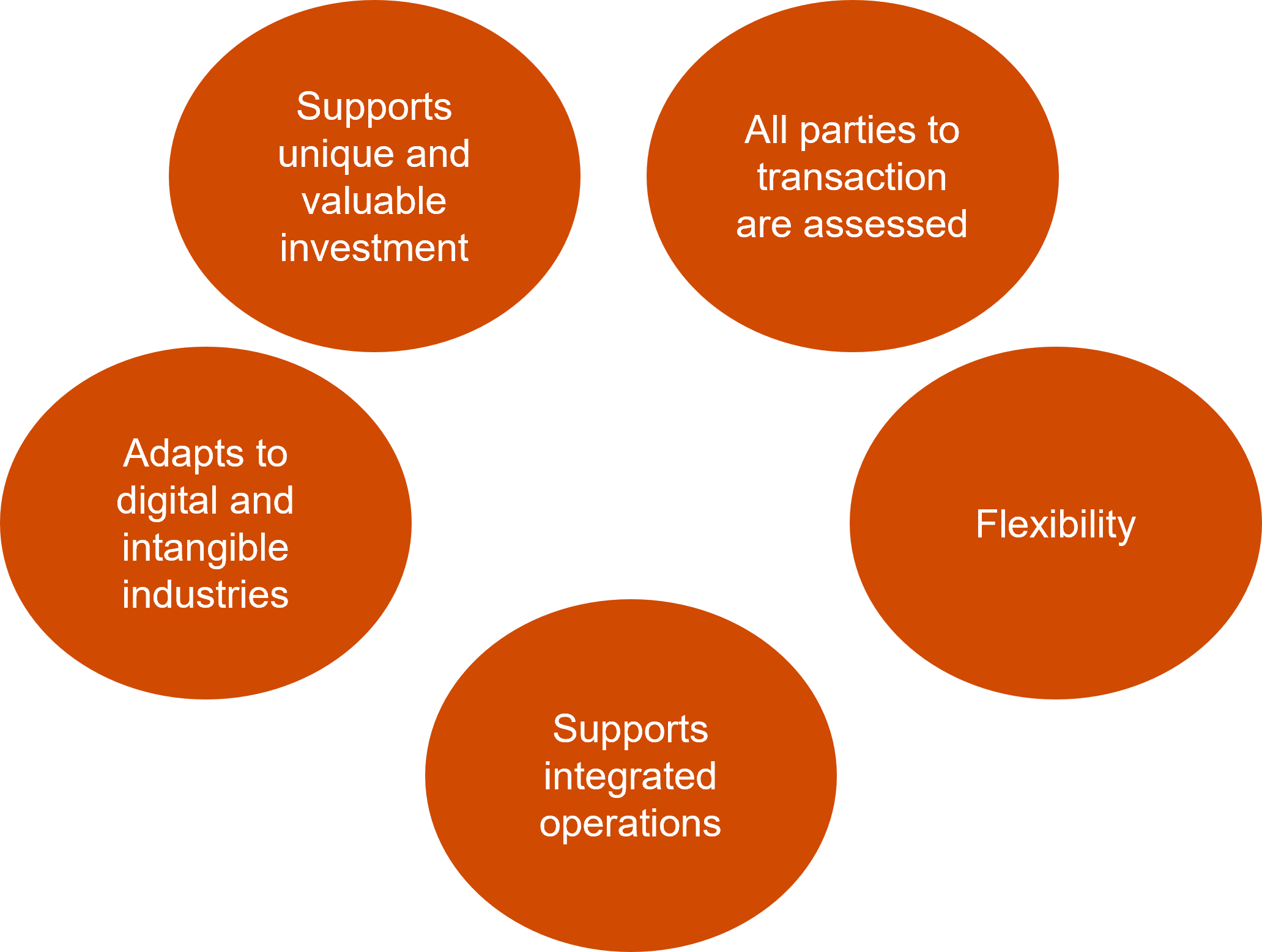

PSM offers a solution where both parties to the transaction make a unique and valuable investment (e.g. in some intellectual property or a trademark). PSM recognises the investment made by each company involved in the transaction and considers it in allocating the profit.

PSM is best used where the activities carried out in related-party transactions are very integrated and the MNE units are working closely together, while having independent functions, risks and assets. In arriving at the profit to be split between the related parties, it’s important to consider each company’s investment in the value chain, which is usually difficult to assess using other TP methods.

It’s important to note that PSM has particular advantages in certain industries, for instance, to determine the investment and profit in companies whose core business activity is closely linked to digital services or creating (improving) intellectual property. The digital services industry tends to have a complex value chain and, as stated above, PSM allows functions, risks and assets to be split so that each company receives an appropriate fee for the functions it has performed. A taxpayer who applies PSM correctly may rest assured that important assets (e.g. intellectual property, software and customer data) and unique risks (e.g. cybersecurity, data privacy and technology changes), which may be a key factor in setting and splitting the fee between the companies, will be identified and taken into account.

PSM is a flexible method capable of considering a wide range of factors, including intangible assets, risks and functions, so it can be used in practically any controlled transaction to show how the true value is created and what fee is payable to each company.

Overall, PSM helps us evaluate all the parties to a transaction and determine the investment each company has made or planned, resulting in each being paid a fair fee at arm’s length.

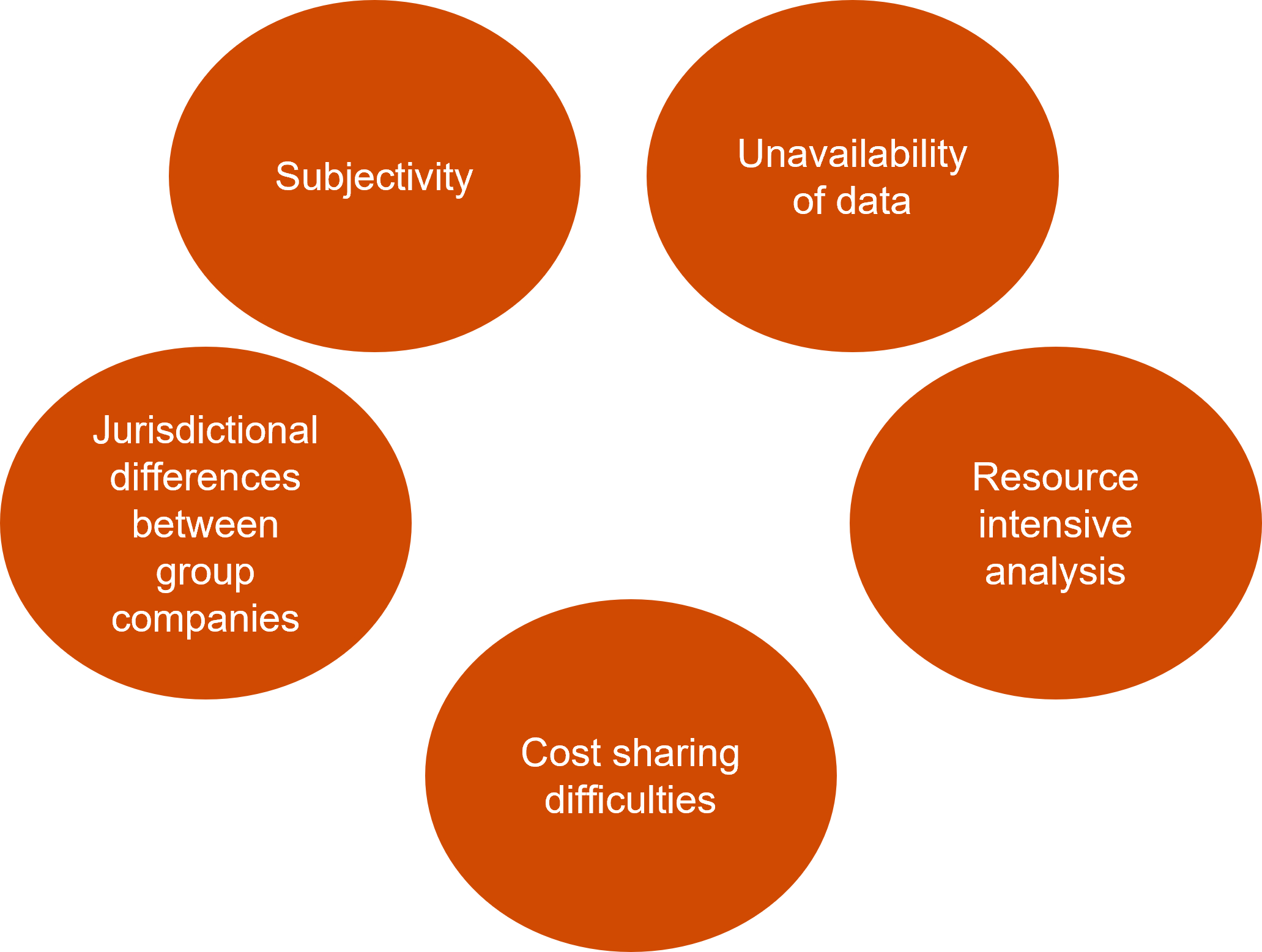

PSM is a subjective method that can raise a lot of questions. It may be interpreted in different ways, potentially causing disagreement between the taxpayer and the tax authority with relevant consequences. Even a slight confusion in identifying functions, risks and assets may lead to widely different results, which may affect profits and each party’s taxable base.

When analysing each company’s investment, it may be difficult to obtain the necessary data from all the companies involved. Even if the data is available, practical difficulties may arise from accounting discrepancies between different jurisdictions, which may affect the taxpayer’s ability to correctly split the profit between the companies involved.

Practical difficulties may also arise from segmenting the parties’ revenues and costs, which is a necessary exercise to arrive at revenues and expenses related to the transaction being analysed by PSM after separating those from other activities unrelated to the transaction under review (companies may carry out a number of business activities).

There are cases where an MNE chooses to apply PSM to its entire value chain. However, as we know, functions, risks, assets and investments tend to vary even within the same MNE whose units have the same functional profile, which may lead to PSM being applied incorrectly in certain jurisdictions and companies receiving fees that do not match their actual functions, risks and assets.

Overall, PSM may be a complex and resource-intensive method. It may lead to disputes with the tax authorities, followed by a costly and lengthy process of settlement, because this method is not universal and not suitable for every industry and every transaction. In particular, PSM is not suited for MNEs with a simple value chain and straightforward transactions.

PSM is a future-oriented solution that fits the complexity of certain business arrangements. This method promotes transparency and can mitigate the risk of profit shifting. It’s a good solution for MNEs with complex value chains seeking arm’s length compliance, but it has certain disadvantages that limit the scope for using it as a universal TP method in analysing related-party transactions. Because of its complexities and other industry-dependent restrictions, PSM is now rarely used in TP analysis, yet we expect it to be used far more often in the future.

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question