We have analysed the CIT treatment of doing business with companies on the blacklist of uncooperative tax havens earlier. This article explores new changes to the list and how they affect transfer pricing (TP).

Recent months have seen repeated changes to the blacklist of uncooperative tax havens due to geopolitical risk pressures.

From 1 November 2023 the list again includes Antigua and Barbuda, Belize and Seychelles because these jurisdictions have failed to share tax information on request.

The British Virgin Islands has been delisted after improving its rules for sharing information on request to meet the OECD standard.

Costa Rica, too, is off the list – the EU Council finds this country has successfully restructured its tax exemption scheme for foreign-source income and eliminated some harmful conditions.

Another delisted jurisdiction is the Marshall Islands, which has made excellent progress in meeting the economic substance requirements.

So the updated list now has 16 jurisdictions, including Russia, which is subject to a toxic preferential tax scheme for internationally sanctioned state holding companies and persons close to them.

Recognising Russia as an uncooperative tax haven has raised the question of TP compliance in taxpayers that are still doing legal and transparent business with non-sanctioned Russian companies despite the massive boycott, their decision to stay in the Russian market being based on humane considerations and rational calculations.

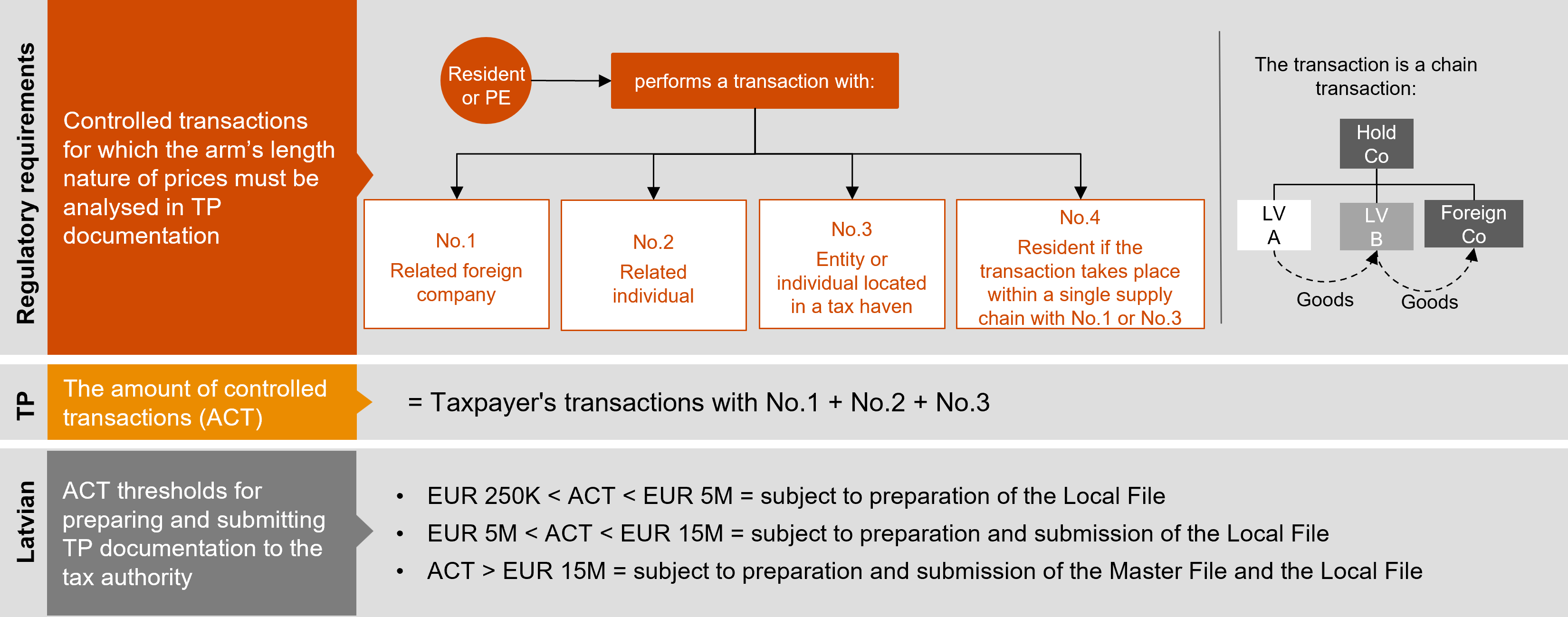

Latvian TP rules list four cases that require a taxpayer or a permanent establishment to assess the need to prepare and submit TP documentation, i.e. whether they do any business with:

The picture below shows how Latvian TP requirements apply:

Traditionally, all cases involve calculating the total amount of goods and services acquired and supplied. A taxpayer that exceeds the first threshold of EUR 250,000 must prepare a local file and submit it to the State Revenue Service on request. Exceeding the second threshold of EUR 5 million requires the taxpayer to prepare and voluntarily submit a local file within 12 months after the end of the relevant financial year. Once his total transactions reach the third threshold of EUR 15 million, he is liable to submit a master file, too.

One thing to note is that the first three cases are about related-party transactions. When it comes to doing business with companies from uncooperative tax havens, including Russia, it no longer matters whether they are related or unrelated. With Russia on the blacklist, a taxpayer doing business with Russian companies may face a higher TP risk from 2023 if he fails to assess his obligation to document TP compliance of his transactions early on.

In such cases a Latvian taxpayer is required to demonstrate arm’s length compliance for any transaction with any Russian-registered entity or individual.

As the deadline for submitting TP documentation in companies with the standard financial year is 31 December (for the previous reporting period), we encourage you to get in touch with our transfer pricing team or email your questions to lv_transfertcenas_info@pwc.com to find out more about your obligations arising from the tax and TP regulatory requirements.

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question