Transfer pricing (TP) experts of the State Revenue Service (SRS) have agreed to meet up with Latvian TP consultants on several occasions in late September to debate some pressing TP concerns and to set out the SRS opinion on how to solve current and future TP problems. In this article we will outline SRS comments on TP validation and look at some of the topics and questions put up for debate with the SRS.

There are plenty of multinational enterprises (MNEs) doing business in Latvia – taxpayers entering into controlled transactions with related parties. The arm’s length nature of those transactions needs validation in order to correctly measure the taxable base for corporate income tax purposes.

To validate TP, taxpayers use a TP file the group has created centrally, which often fails to give all the significant information required by the Latvian rules, or its benchmarking study permits different interpretations.

In TP disputes with the SRS, taxpayers often argue that the tax authorities of other countries have recognised a particular approach to validating TP in the group file. The SRS then makes it clear that Latvian taxpayers are bound by the tax policies and rules adopted by Latvia.

Even the information in TP files created in collaboration with Latvian TP consultants is often recognised by the SRS as inadequate, and the SRS frequently disagrees with the approach taken in benchmarking studies and challenges the selection of comparable companies.

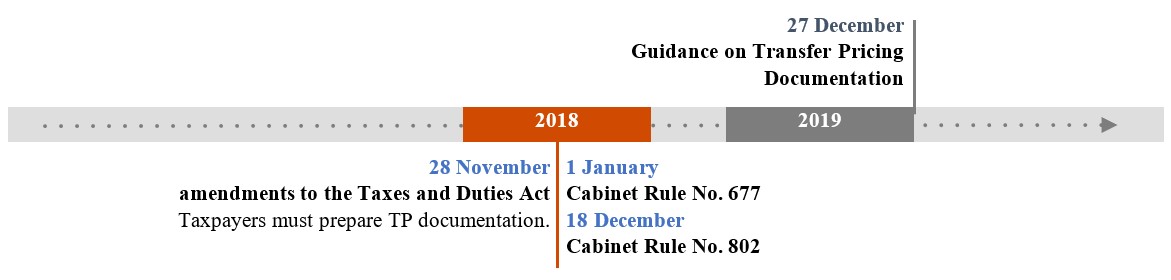

What is the relevant legislation that includes TP rules and gives the taxpayer legal certainty about TP, the amount of information and the approach? Below is the legislation that lays down requirements for TP validation and the only guidance published by the SRS:

It’s important to note that recommendations made by the OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations, the most influential source of TP instructions, can be used by taxpayers only as an auxiliary source and only in certain cases.

The sad conclusion is that the local TP rules are neither comprehensive nor unambiguous and this leaves TP open to interpretation. There are many key questions that the available information fails to answer, and there are no other sources of reference that taxpayers could access.

For this reason we entered into active correspondence with the SRS about communication to find out their vision for various TP situations facing MNEs in Latvia.

The main aim of this communication is to obtain an in-depth understanding of topics on which there is a difference of opinion among the consultants and in communication with the SRS, and to clarify the confusing regulatory requirements and explanations offered in the SRS guidance, which in certain situations give taxpayers freedom of interpretation.

For example, one of the questions is how to treat cash-pool and credit-line transactions and their amounts in the TP file. The SRS guidance explains that if a taxpayer makes a large number of cash-pool transactions during the financial year but the financial transaction’s year-end balance is zero, the SRS interprets this as no transaction. Yet it’s debatable whether this conclusion gives a fair view of the transaction taking place in the financial year.

Another example is the taxpayer’s obligation to state the total value of transactions on informational lines 6.5.1 and 6.5.2 of the corporate income tax return for the last month of the financial year before audited results for the period become available. Such preliminary information is not accurate, and in most cases the taxpayer ends up needing to adjust those lines.

While the consultants have put together a list of questions, it needs to be stressed that this communication is intended as a discussion to exchange opinions and debate issues around TP, risks and possible solutions for the present and the future.

This is a big step forward in working with the SRS to reach an understanding, minimise uncertainty and find uniform solutions for a more transparent documentation of controlled transactions, as well as mitigating taxpayer risks in defending their TP and preparing their files.

In our upcoming articles we will keep you informed of any new insights we gain during these meetings. If you have any questions about TP topics please get in touch with our TP team.

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question