It’s been quite a while since Latvia adopted new transfer pricing (TP) rules, yet the State Revenue Service (SRS) did not issue guidelines on charging fines for breaches of requirements for duly submitting or preparing TP files until late September 2023 (approved by SRS order No. 201 of 11 September 2023). This article explores the new guidelines.

The requirements for preparing TP files and submission deadlines are governed by section 15.2 of the Taxes and Duties Act. The content of information to be included in a TP file is detailed by the Cabinet of Ministers’ Rule No. 802 “Transfer pricing documentation and procedures for entering into an advance pricing agreement between the taxpayer and the tax authority for a transaction or type of transaction”.

According to the principles of administrative procedure, on detecting non-compliance, the SRS has the power to charge a fine under section 15.2(14) of the Taxes and Duties Act:

The lawmaker has given the tax authority discretion to decide whether an administrative instrument should be issued and a penalty charged.

Over the last two years, PwC’s TP practice has seen the SRS occasionally fining taxpayers who committed a material breach of Latvian TP requirements, yet there was a lack of certainty as to how fines can be individualised in proportion to the breach.

The guidelines aim to drive uniform administrative practices and provide a common understanding of the statutory criteria for charging fines and achieving proportionality, as well as to avoid charging an identical fine for breaches of different significance.

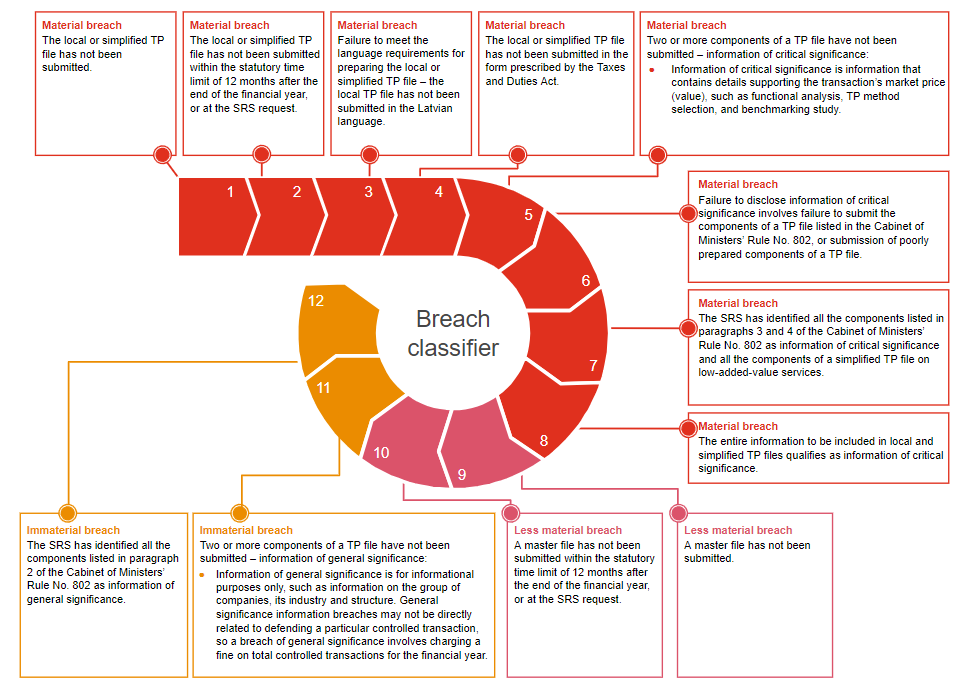

The guidelines classify TP breaches as material, less material and immaterial:

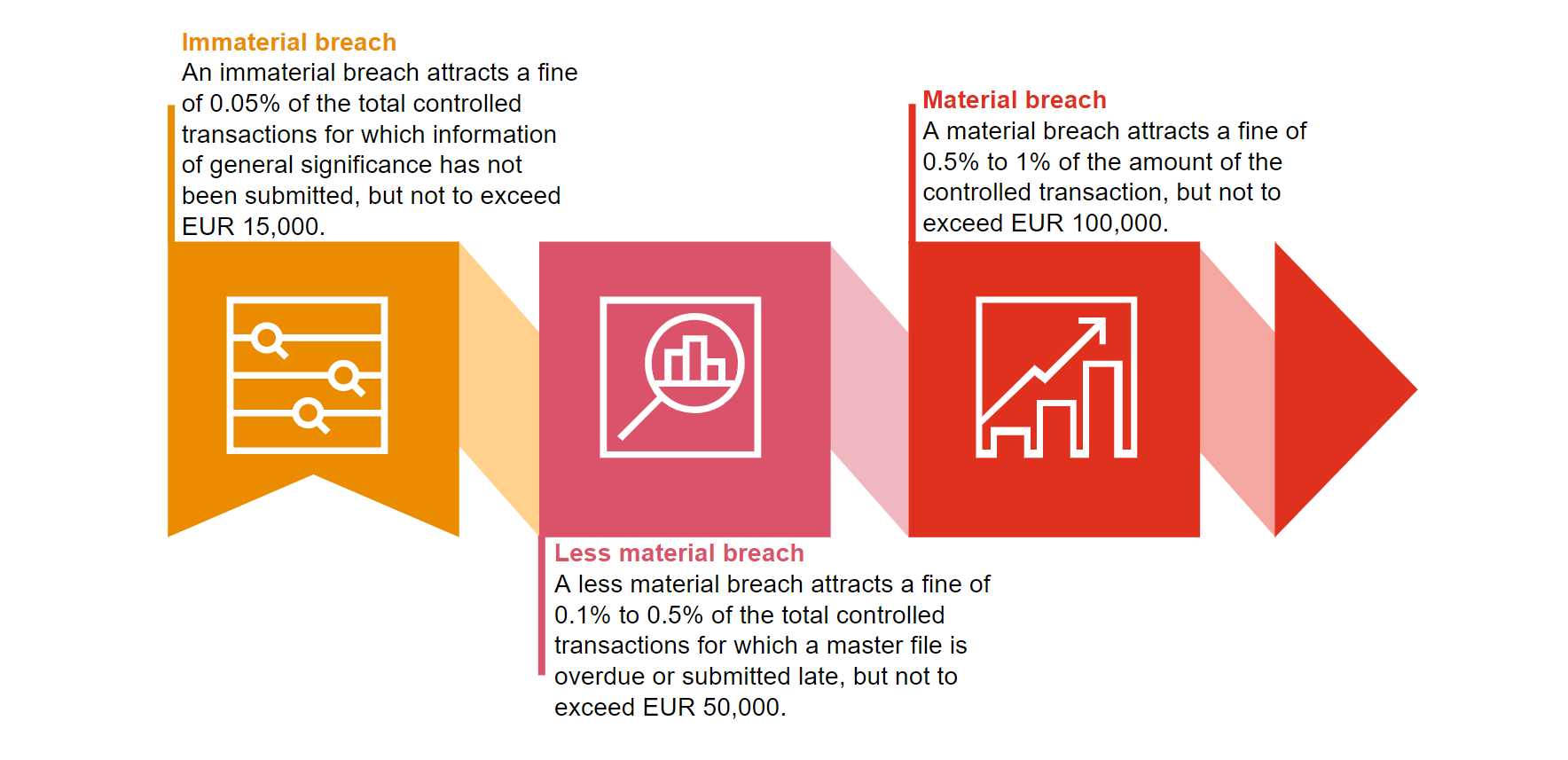

The guidelines provide that the SRS will determine the amount of a fine according to the breach and the taxpayer’s individual assessment:

It’s essential to note that the SRS will consider the taxpayer’s individual assessment to be calculated according to the guidelines. The taxpayer’s individual assessment calculation will take account of the percentage value increasing or reducing the fine, as well as any aggravating or mitigating circumstances.

If two or more breaches (immaterial, less material or material) are detected for the financial period, the SRS will assess each breach on its merits and charge a fine for each separately. The good news is that the guidelines state that the total fine for all breaches charged by the SRS will not exceed EUR 100,000.

It’s also important to note that the guidelines will be invoked in hearing appeals against decisions on fines charged before the guidelines came into force.

The new guidelines give the SRS and taxpayers more certainty and a better understanding of how fines will be charged. However, the SRS is expected to carry out TP checks more vigorously once the guidelines come into force.

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question