Our Flash News edition of 17 May 2019 and 23 May 2019 looked at the significance of working capital in a company’s business. This article explores when and why we need to assess working capital in a transfer pricing analysis.

Every company should have sufficient funds enabling it to duly cover staff costs, taxes and accounts payable to suppliers, including costs incurred in transactions with related parties.

A company’s ability to pay off debts arising in the course of business is reflected by its working capital (“WC”), computed as current assets less current liabilities. Efficient use of WC directly affects the company’s profits and cash flows.

Every company plans its WC cycle—the number of days from ordering inventories to receiving cash for sales. The longer this period, the more the company has to earn to finance its inventories and other business costs. This has to do with the time value of money being driven by various factors, for example:

Accordingly, the later we receive cash for the goods/services sold and the earlier we pay our suppliers, the more money we need to invest in financing our WC. So the size, availability and financing of WC required for business directly affects our profit. And that is when WC might affect the transfer pricing analysis since examining a Latvian company’s transactions with related parties for compliance with the arm’s length principle often involves assessing the profit margin the Latvian company (“tested party”) earns in its related-party transactions. As part of the transfer pricing analysis, the tested party’s margin is compared with margins earned by comparable independent companies making up the arm’s length range. If the tested party’s margin is within the arm’s length range, its related-party transaction can be recognised as arm’s length.

If the tested party’s business is sufficiently similar to the business of selected independent companies, the question of WC does not usually arise because this indicator, too, should be comparable with other companies. However, there are also different cases:

If the business done in the tested party’s controlled transactions substantially differs from the business done by comparable companies, we need to consider whether this difference is reflected in the WC cycle. If the answer is yes, we should consider the need to make a WC adjustment to the arm’s length range.

The OECD’s Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations1 recommend a WC adjustment when it comes to assessing the value of timing differences between the tested party’s profit margin in its controlled transactions and the margins of unrelated parties in a comparable business and determining an adequate fee for financing the goods/services concerned. This recommendation assumes that the profit should reflect these differences, as the company needs funding to cover the space between investing money (i.e. payment to suppliers) and recouping money (i.e. payment from customers).

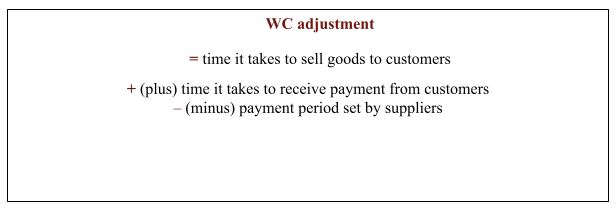

The timing difference is computed according to this formula:

The OECD guidelines describe how a WC adjustment is computed in the following steps:

______

1OECD guidelines, paragraph 3.49 and Annex to Chapter III: Example of a Working Capital Adjustment

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question