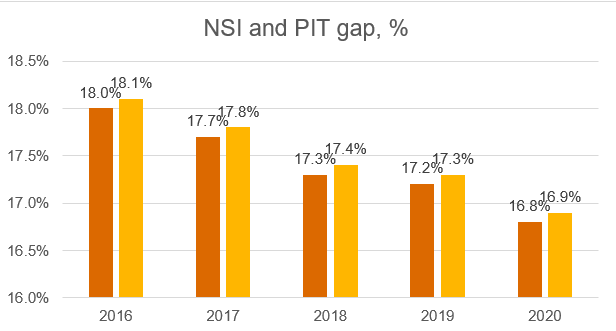

The payroll tax gap has tended to diminish slowly but surely since 2016, according to a 2020 national social insurance (NSI) and personal income tax (PIT) gap assessment recently carried out by the State Revenue Service (SRS).

The tax gap means all amounts of tax that go unreported and taxes that are reported but remain unpaid in comparison to the potential total that would be assessed and collected if all taxpayers paid their tax liabilities in full. The tax gap is affected by a number of factors such as:

The SRS uses the tax gap analysis for the following purposes:

The SRS has measured the tax gap (unreported employment pay) for the fifth consecutive year. In 2020 the rate of unreported pay was 17.1%, a reduction of 0.2 percentage points on 2019. According to the SRS, in 2020 the net unreported pay was EUR 903.73 million, while the NSI and PIT gaps were EUR 445.23 million and EUR 198.14 million respectively, i.e. the government missed a total of EUR 643.37 million.

The study suggests that unreported pay is mostly received by employees in occupations such as chief executive officer, lorry driver, shop assistant, construction worker, and accountant. The risk of unreported pay mostly affected employees aged 55–64 (i.e. persons nearing retirement age).

Overall, the ratio of employees receiving unreported pay to total employees is evenly distributed by region. The highest percentage of workers receiving unreported pay is found in Riga (32.1%) and its suburbs (30.4%), where the highest economic activity is observed.

The SRS believes that the payroll tax gap reduction in recent years is due to tax control measures taken by the SRS, but the study unfortunately omits to mention which of those measures have been the most effective.

Link to the SRS study and press release.

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question