Given the current challenges facing Europe—ranging from increasing geopolitical tensions and slowing economic growth to intensified global technology competition—the European Commission (EC) has concluded that the European Union (EU) requires a comprehensive business plan that integrates climate action, circularity, and competitiveness.

On 26 February 2025, the EC presented the Clean Industrial Deal1 (CID), a strategic plan designed to accelerate decarbonisation, re-industrialisation, and innovation while enhancing the competitiveness of EU industries. The CID aims to strike a balance between the EU's global competitiveness and its ambitious environmental goals outlined in the Green Deal.

Achieving the objectives of both the Green Deal and CID is not possible without a strong industrial base. To bolster industry and competitiveness, the EU must have immediate access to capital. As part of this strategy, the CID will focus on mobilising EU-level funding, attracting private investments, and enhancing the state aid framework.

As part of the CID, the EC is set to adopt a new State Aid Framework2 by June 2025 to accelerate and simplify the deployment of renewable energy, expand industrial decarbonisation, and ensure sufficient capacity to produce clean technologies.

The CID focuses mainly on two closely related areas:

Another key element of the Clean Industry Deal (CID) is circularity, which focuses on optimising the EU's scarce resources and reducing excessive dependence on third-country suppliers of raw materials.

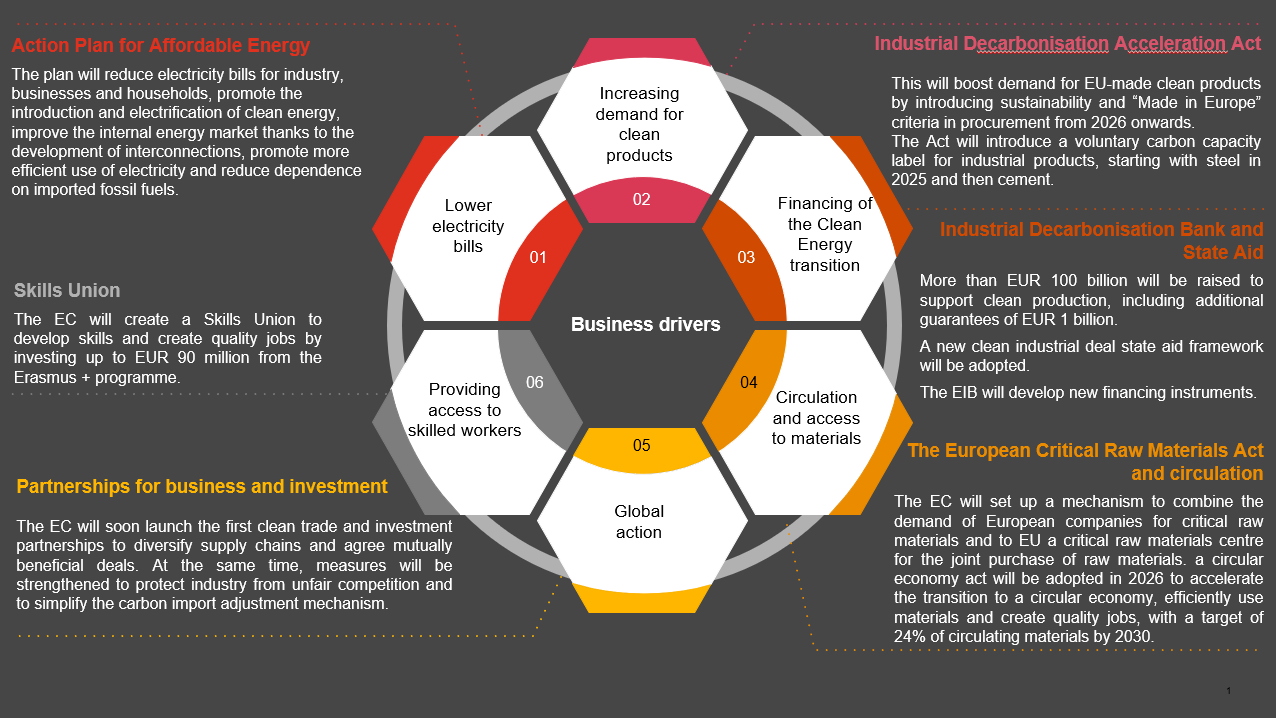

The CID highlights six main drivers of entrepreneurship that contribute to the development and growth of industrial sectors within the EU (see the Figure below).

Tax incentives play a crucial role in the CID, aiming to promote electrification and reduce dependence on fossil fuels. Member States are urged to finalize negotiations on the Energy Taxation Directive, which would enable tax reductions for energy-intensive sectors. The European Commission (EC) will issue recommendations on tax reductions and the harmonization of network charges. Additionally, the EC will advise Member States to review their corporate tax systems to incentivize investment in clean technologies, such as offering shorter depreciation periods and tax benefits in strategic sectors.

The CID offers companies new opportunities to attract finance and develop sustainable entrepreneurship. However, while the potential is high, navigating changing circumstances and regulatory changes and identifying associated risks, such as regulatory, financial, competition and contract risks, can be a challenge. In such a situation, legal advice can be very useful. PwC subject-matter experts will be happy to provide you with the support you need to adapt to these changes and make the most of the opportunities offered by the CID.

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question