Communicating with the State Revenue Service (SRS) is certainly the safest way to make sure the interpretation of law we use daily complies with how it was originally intended.

Most of the guidelines published by the SRS explain clearly how statutory requirements should be applied. Yet the 2019 guidelines on transfer pricing (TP) documentation offer a formula for computing the amount of a controlled credit-line or cash-pool transaction made in the financial year that gives the taxpayer much more room for interpretation. This alternative formula became the subject of debate again in recent communication between TP professionals and the SRS.

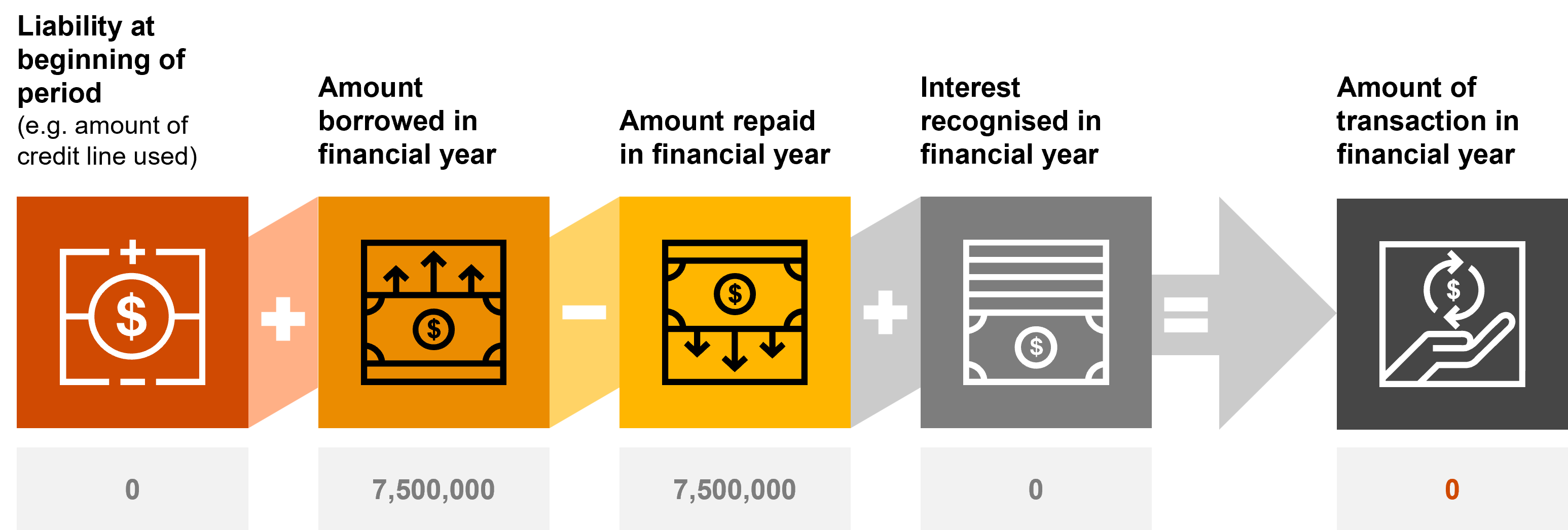

According to the SRS guidelines, the calculation of the controlled transaction amount (CTA) of a loan (including a credit line) is based on the amount borrowed or lent and interest charges recognised in the financial period, while the alternative formula is permitted in a credit-line or cash-pool transaction.

The alternative formula was created to reflect the facts and circumstances of each contract and the large number of transactions when a loan is received and repaid, which prevents the true amount of the intragroup financing transaction from being reflected objectively enough.

For these reasons and given how controlled transactions of a revolving credit line and a cash pool differ from normal loans, in determining the CTA of a credit-line or cash-pool transaction, the SRS guidelines allow taxpayers to interpret the language ‘amount of transactions in the financial year’ found in section 15.2 of the Taxes and Duties Act, which requires the taxpayer to prepare and submit a TP file, as an arithmetic expression:

According to the alternative formula, if the taxpayer repays the amount borrowed one day before the end of the financial year and the transaction balance on the last day of the financial year is EUR 0, then the CTA for the financial year is exactly EUR 0. This leads us to doubt whether the alternative formula provides a true and fair view of the controlled financing transaction and CTA for the financial year.

This interpretation of the CTA for a credit-line transaction is certainly favourable to the taxpayer. Yet lines 6.5.1 and 6.5.2 of the corporate income tax return relating to controlled transactions and CTAs with related non-residents and residents respectively are only completed on the tax return for the last tax period, which widens the scope for interpretation:

In June 2024, the TP professionals communicating with the SRS repeatedly brought up the issue of the alternative formula and asked the following questions:

The SRS gave a politically correct answer that this approach to computing the CTA of financing (credit line and cash pool) transactions has been approved by the Finance Ministry, and the approach was chosen and the formula created to ease the administrative burden on the taxpayer.

The SRS answered that no recommendations are expected for computing the CTA of credit-line and cash-pool transactions for the financial year.

The SRS’s answer means that the alternative formula for computing the CTA of a credit-line or cash-pool transaction stands and the scope for using it still primarily depends on the taxpayer’s interpretation. The taxpayer subjectively decides on what the transaction’s facts and circumstances should be and what should qualify as a sufficiently large number of transactions to use the alternative formula.

This issue was raised by our colleagues in 2019 as a potential subject for repeated debate, but this topic is still relevant and will come up in our further communication with the SRS.

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question