As technologies keep evolving, we often hear about new tools of artificial intelligence, business intelligence, data processing, analysis or visualisation and the opportunities they offer. These technology solutions can help companies make fast and efficient decisions and manage their processes transparently. Transfer pricing (TP) has been evolving in this respect as well. The opportunities offered by various technology tools can help companies standardise, automate and rationalise their processes associated with TP management and compliance, an area known as operational transfer pricing (OTP). This article explores what the new concept means and what opportunities it offers.

OTP is not just another amendment to the TP guidelines or local rules that puts an extra burden on taxpayers. We should embrace this as an opportunity resulting from technological advances in symbiosis with TP. OTP is a set of technology-based TP solutions that help companies properly implement their TP policies and meet their operational challenges. OTP solutions can be used to strategically develop, evaluate and report on TP-related opportunities, threats and compliance issues. We as TP consultants are able to provide and implement these services in your organisation.

When communicating with our clients or facing large volumes of data coming in from a particular client, we have noticed that:

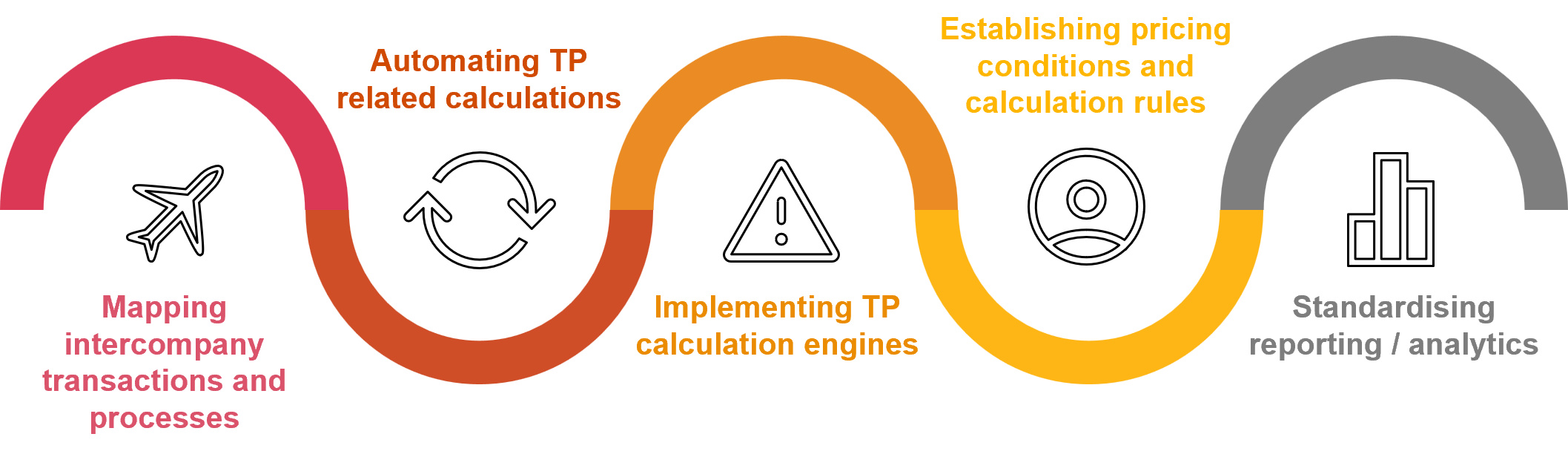

If you recognise some of these issues or if your company struggles with them frequently, solutions resulting from OTP services are able to solve them. The image below shows the main ways OTP solutions can facilitate processes associated with TP management and compliance.

Since every company’s core business is unique and each company has its own special needs, today’s technology solutions are easily tailored for all kinds of TP needs and goals. In developing automated tools, you can use comparatively simple Microsoft Excel spreadsheets along with Microsoft Power BI data aggregation and visualisation goals. For example, it’s possible to develop a segmentation of your financial data that helps you analyse your revenues and expenses in transactions with related and unrelated companies and your profit indicators in each line of business. Such a simple yet transparent solution helps you better understand your company and make strategic decisions that will improve your business. It’s also possible to develop far more complex automated tools that will, for instance, gather internal data, extract data from public databases, process the data with the Alteryx tool, and integrate the solution into your company’s internal IT system, such as SAP. These solutions allow you to track the TP on your transactions in real time or periodically (weekly, monthly or quarterly) so you can make efficient decisions and implement changes. This helps you avoid situations where you find at the end of the financial year that the TP on your transactions with related parties is inappropriate and an adjustment is required.

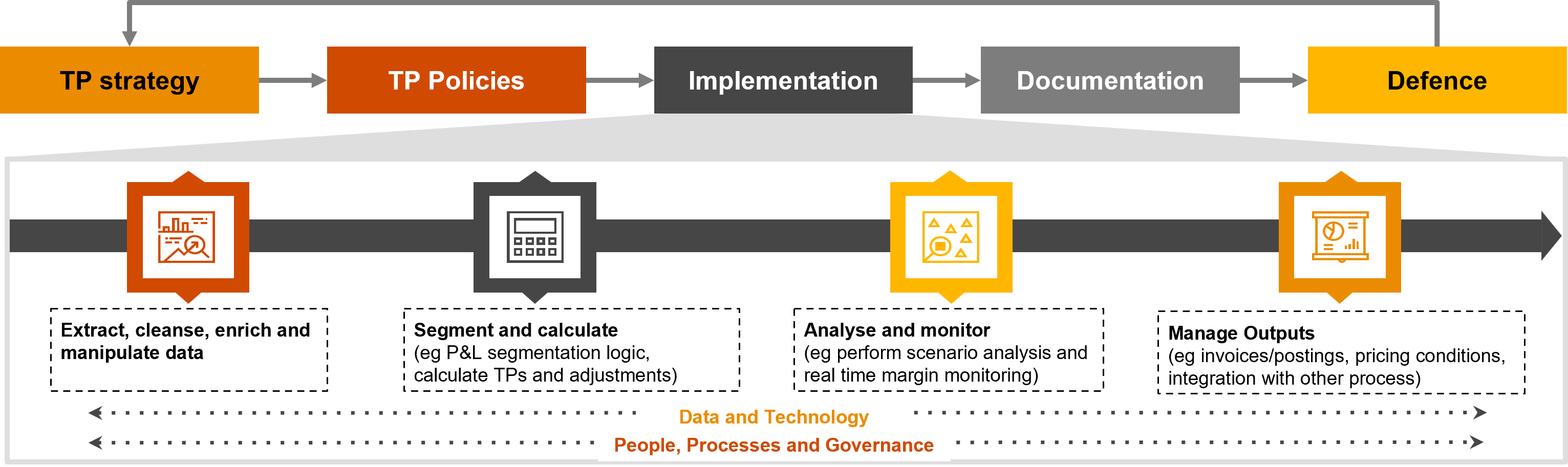

OTP is a solution that can support companies across all aspects of TP implementation.

Today’s technology offers opportunities to develop tools for various companies and specific needs. While the development and implementation of certain automated solutions can initially demand considerable human resources, time and money, they will definitely bring benefits and allow you to tackle tasks with high added value in the long term, especially in companies that are taking part in intragroup transactions and whose TP analysis involves analysing large volumes of data.

PwC Latvia’s experience in dealing with non-standard TP issues, backed by PwC’s global network of companies and expertise, allows us to identify, develop and implement tailored OTP tools. If your company is interested in discussing the opportunities that such automation offers or how you can manage your TP compliance, please reach out to our TP team.

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question