We have written earlier about the State Revenue Service (SRS) pointing out significant errors in transfer pricing (TP) files and focusing on the lack of financial data segmentation, the tested party or its financial data, and the benefit test (i.e. evidence of services). This article explores some other common breaches.

According to TP requirements defined in section 15.2 of the Taxes and Duties Act and applicable from 1 January 2018, an entity subject to corporate income tax must provide evidence that a related-party transaction (‘controlled transaction’) is arm’s length in the master file and the local file, or only in the local file, by including information specified by the Cabinet of Ministers’ Rule No. 802.

More and more companies choose to prepare uniform TP files at group level, which helps the group save money and allows all the companies to take a single approach to preparing their TP files. Local TP requirements are often ignored in such situations, which increases the risk of penalty. The penalty for breaches in the content and language of TP files is particularly material for Latvian-registered companies because it may reach EUR 100,000. To mitigate this risk, before submitting a TP file to the SRS, you should make sure it contains all the required details and rectify any shortcomings you have identified.

Let us now look at some common breaches.

One of the main breaches is using a language that fails to meet statutory requirements. Section 8(4) of the National Language Act states that statistical reports, financial statements, accounting documents and other documents to be filed with national or municipal institutions under a law or any other enactment must be drawn up in the national language (Latvian). This Act applies to the local file as well. If the taxpayer submits the local file to the SRS, say, in English, the SRS may charge a maximum penalty of EUR 100,000 even without assessing the contents.

It’s important to note that Latvian TP rules (section 15.2(13)(3) of the Taxes and Duties Act) make a language exception for the master file, which may be prepared in Latvian or English.

Another breach we have written about earlier has to do with the taxpayer being allowed to revise TP files and the comparables used in them every three years. Section 15.2(5) of the Taxes and Duties Act states that the local file and the comparables used in it may be revised every three years only by taxpayers whose total controlled transactions for the financial period are up to EUR 5 million. If total controlled transactions exceed this threshold, the taxpayer is required to update the entire information disclosed in the local file and prepare a new benchmarking study every year.

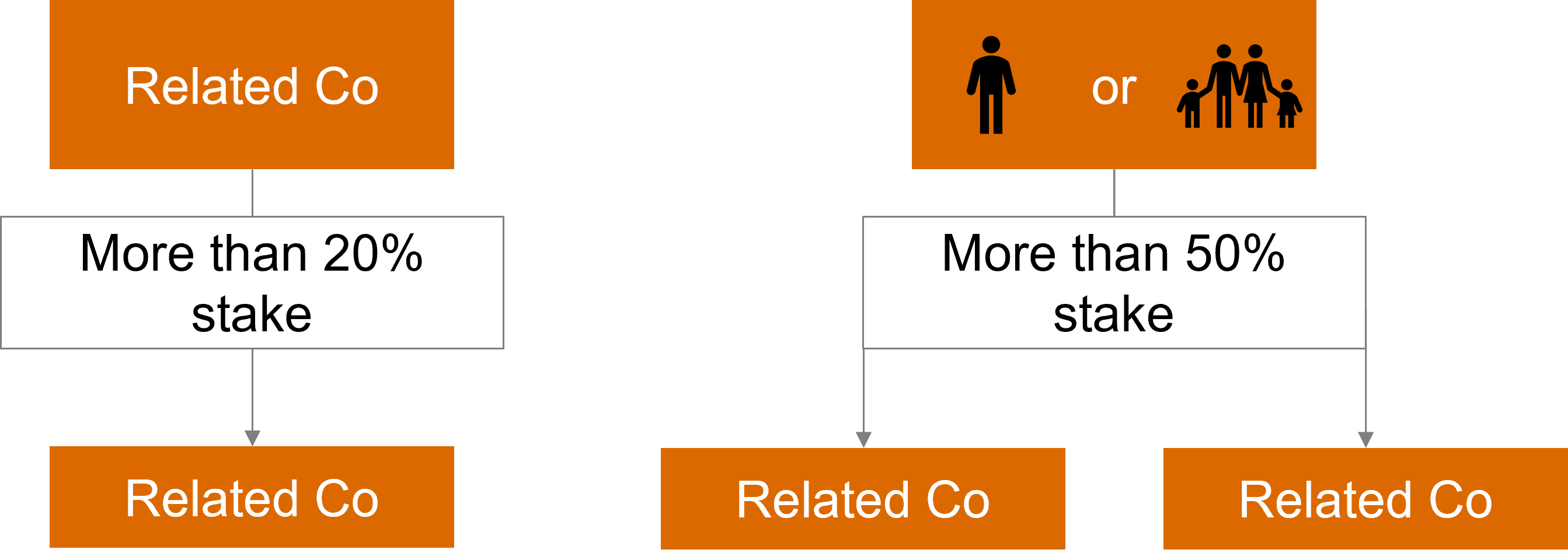

The next common breach arises when the independence threshold is determined in a benchmarking study. Given the independence threshold prescribed by Latvian legislation (section 1(18) of the Taxes and Duties Act), companies are considered independent if the stake an entity or individual holds in another company, whether directly or indirectly, does not exceed 20% or 50% respectively. Applying this condition means the benchmarking study might include companies that are not independent.

When it comes to conducting a TP analysis and determining an arm’s length price, it’s important to provide high-quality comparables. This involves carefully choosing the size of the dataset, for instance, using the financial indicators of comparable companies for one year or more years. Since other countries mandate the use of average indicators for three years, Latvian companies often apply this foreign practice in defending their arm’s length prices. However, Latvian TP rules favour the latest available financial data for one year. Paragraph 3.2.9 of Rule 802 states that if a benchmarking study uses data for multiple years, the company must give legitimate reasons for taking this approach.

As we have written before, there are certain differences between the Baltic States in defining a material transaction. It’s EUR 20,000 in Latvia and EUR 90,000 in Lithuania, while Estonia permits taxpayers to decide which of their transactions are material.

Given Latvia’s low threshold for a material transaction, TP files prepared by the group often fail to include a Latvian company’s transactions with a related non-resident and consequently there is no evidence that those transactions are arm’s length.

In addition to the errors and breaches described above, the local file often omits some other details required by Rule 802, such as copies of agreements for controlled transactions, a description of critical assumptions, or a list of payments made and received. Any of these omissions could be enough for the SRS to consider launching an in-depth TP review, which may lead to a penalty being charged. To mitigate the risks inherent in your master file or local file being prepared centrally, we recommend you revise it and make any necessary amendments to ensure it meets the local TP requirements.

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question