Much of the acquisition cost in a share deal tends to be financed externally, i.e. by borrowing. Repayment of a shareholder’s loan is typically exempt from corporate income tax (CIT) under Latvian law (more details in our article CIT reform: lending to related parties). Also, if interest paid on the shareholder’s loan complies with Latvian thin capitalisation rules and transfer pricing rules and is used for business purposes, i.e. it qualifies as a business expense, the interest charges are exempt from Latvian CIT.

Where interest charges exceed the thin capitalisation threshold, the excess is subject to CIT at an effective rate of 25%. If the level of interest is not arm’s length for transfer pricing purposes, the excess over an arm’s length level will also attract CIT.

Net interest expense of up to EUR 3 million

Companies in which the difference between their annual interest expenses and interest income does not exceed EUR 3 million should apply the equity method prescribed by section 10(1) of the CIT Act. This means increasing the taxable base proportionally by interest whose average liability exceeds four times the shareholders’ equity (except for reserves) at the beginning of the year.

This method does not apply to interest paid on loans from a financial institution meeting the following criteria:

Net interest expense of more than EUR 3 million

Companies with net annual interest exceeding EUR 3 million must pay CIT on the excess interest expense using one of two methods:

If both methods result in an increase, only the higher amount should be added.

It’s also important to note that section 10 of the CIT Act prescribes a few exceptions for exempt loans.

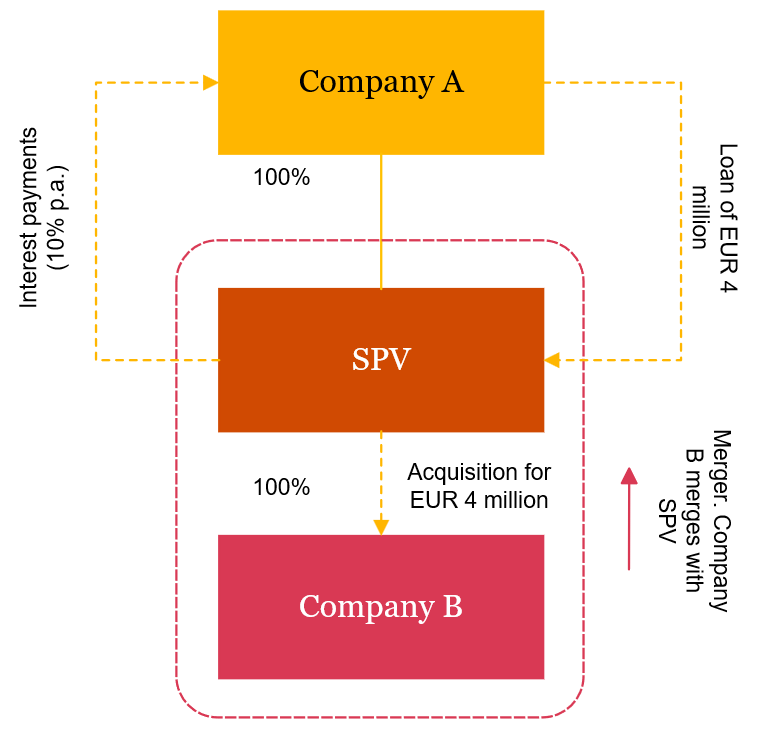

It was standard practice to use debt pushdown in restructuring deals a couple of years ago. This typically involved setting up a special purpose vehicle (SPV) that received a loan to directly acquire shares in a target company.

The newly acquired target later merged with the SPV (i.e. the target’s shareholder). The tax benefit from this restructuring process was that the target’s income could be reduced by deducting interest charges on the loan that was used to acquire shares in the target itself (more details in the next article).

While there are no legal obstacles to using a debt pushdown structure, it has a number of tax implications and is internationally viewed as aggressive tax planning. Let’s look at an example to better understand the situation.

Company A incorporates an SPV primarily to acquire Company B, the target, for EUR 4 million. To provide adequate financing for the acquisition, Company A lends EUR 4 million to the SPV at an interest rate of 10% per annum. After the acquisition, Company B is to merge with the SPV.

A step plan for the deal structure

On completion of the structuring deal, the group consists of two companies: Company A and the SPV (with Company B merged into it).

This poses the risk of the State Revenue Service (SRS) claiming that the transaction (i.e. lending to the SPV to acquire Company B, with the target later merging into the SPV) leads to a debt pushdown structure, which is recognised as aggressive tax planning.

This example leads to a structure that helps exclude dividends payable by Company B to the SPV, which would attract 25% CIT effective and be used by the SPV to repay the principal and pay interest.

The post-merger structure means that Company B, which had its shareholder – the SPV – receive a loan to acquire it, is merged with the shareholder, which enables the SPV to repay the principal and interest to Company A, distributing no profit and avoiding Latvian CIT.

While the CIT Act is silent on situations involving debt pushdown, the SRS believes this structure is set up for the sole purpose of reducing the tax base. Accordingly, repayment of the principal and interest payments are deemed profit distributions, with the result that the principal and interest is fully chargeable to CIT (regardless of the thin capitalisation rules).

It’s essential to emphasise that in the absence of public SRS tax rulings or guidelines on structuring similar deals, the Latvian CIT system makes it very likely that the SRS will treat a debt pushdown structure as aggressive tax planning. Building such a structure therefore needs robust commercial or business reasons to mitigate CIT risk.

In summary, if on a tax audit the SRS treats this as aggressive tax planning, the principal and interest will attract 25% CIT effective as well as late fees (0.05% per day on the total tax due, capped at 40% of the tax due). While the tax authorities have the power to charge penalties in full, these can be reduced if the taxpayer enters into an agreement with the SRS on mutual cooperation.

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question