Cashback is one of consumer incentive programmes that are currently popular with manufacturers and wholesalers. This could involve a manufacturer (or a wholesaler) refunding a certain amount of money to the end consumer for buying goods they have manufactured (distributed). The refund may be a fixed price for a particular product or expressed as a percentage of the purchase value. A cashback may also occur as a discount coupon distributed by the manufacturer, which the end customer uses with the retailer, who then seeks reimbursement from the manufacturer. This procedure directly stimulates the end consumer’s choice because the manufacturer’s discount reaches him directly instead of being accumulated in the chain of traders. With many companies expanding their business beyond Latvia, a discount may also be granted to customers in other member states. This article explores whether a cashback made by the manufacturer (wholesaler) to the end customer affects the VAT payable by the manufacturer (wholesaler).

The VAT implications of a payment (cashback, discount coupon etc) granted by the manufacturer to a person that is not the direct party to the manufacturer’s transaction, should be examined in the light of the case law of the Court of Justice of the European Union (CJEU).1 The Latvian State Revenue Service agrees with this approach.

There are several factors we should assess to find out whether this payment allows the manufacturer to reduce the VAT payable to the Treasury.

Under the VAT directive2 the taxable amount of a supply is a consideration which the supplier has received or will receive for the supply from the customer or a third party, including subsidy, that is directly linked to the price of the supply. The amount chargeable to VAT excludes:

Moreover, cancellation, rejection and total or partial non-payment, as well as reducing the price after the supply will all reduce the amount that is subject to VAT accordingly.

Similar rules are laid down by sections 34(1) and 39(1–2) of the Latvian VAT Act.

The CJEU has stated that a cashback, a coupon usable with the retailer and similar bonuses which the manufacturer has granted to a person that is not the direct party to the manufacturer’s transaction, is a discount. And this discount reduces the manufacturer’s taxable amount if it’s granted for goods he has distributed (sold).

The clause of the directive that provides for reducing the taxable amount if the price is reduced on completion of the transaction expresses the core principle of the directive: VAT is chargeable on the consideration actually received and the taxable person cannot be required to pay to the Treasury an amount of VAT exceeding the amount he has actually received for the transaction.3 VAT is basically charged on end consumption. In general, neither the manufacturer nor the wholesaler incurs VAT costs because they merely make up the chain through which the VAT paid by the end consumer reaches the Treasury.

It’s important to note that the manufacturer grants a discount for the purchase made by the end customer, with the result that the cashback or discount coupon contains VAT.

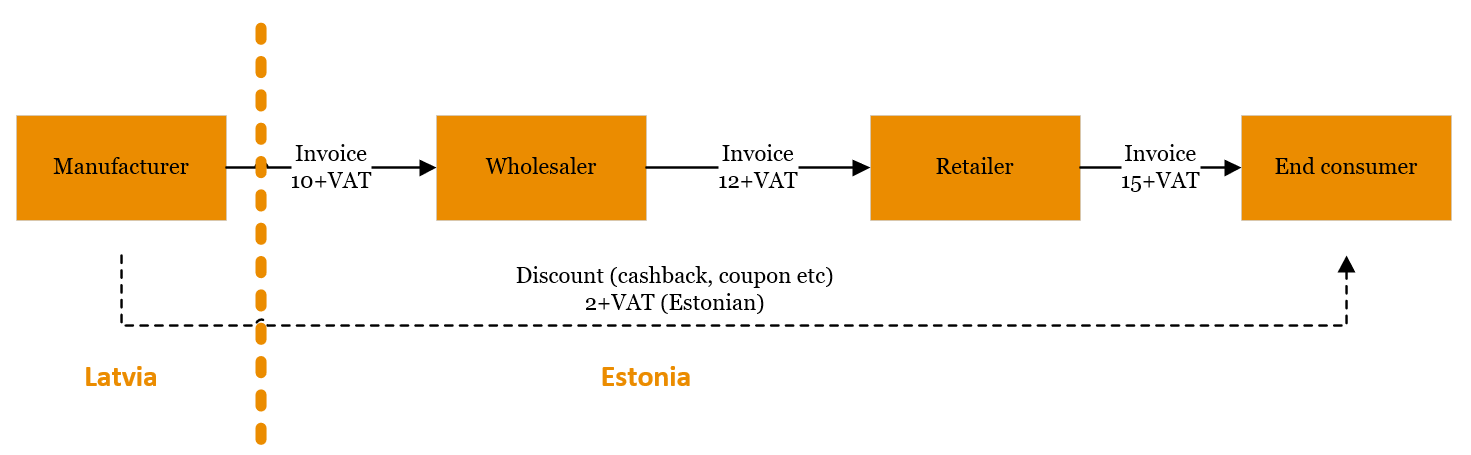

The CJEU finds that for the manufacturer who grants a discount for his goods, but not to the direct party to his transaction, the consideration actually received for the supply of goods is the consideration received from the direct party to the transaction, less the discount granted to the end customer (in our example the consideration received by the manufacturer for the goods supplied would be 10–2=8). The length of the supply chain and the fact that the discount is not granted to the party to the transaction do not change the principle for determining the taxable amount. It’s important that the discount should be granted for goods originally sold by the manufacturer. In other words, we must be able to prove that the discount granted at a later stage of the supply chain is for the goods which the manufacturer supplied at the beginning of the chain.

This VAT treatment also applies to the pharmaceutical manufacturer’s financial participation in the supply of reimbursable medicinal products in Latvia, paid to the National Health Service.

The CJEU states that a discount granted further down the supply chain reduces the taxable amount, yet it may not reduce the VAT charge.4

There is no problem as long as all the supplies take place within one country. The manufacturer reduces his taxable amount charged to VAT at the standard rate (or a reduced rate) and the VAT due decreases accordingly. According to the State Revenue Service, a credit note should be issued to the end consumer.

Problems arise if the manufacturer has failed to charge VAT on the original supply of goods because his transaction is a zero-rated intra-Community supply and not a domestic supply of goods.

By applying a discount, the manufacturer could reduce the taxable amount of the supply. Yet the zero-rating means there is no value of goods charged to VAT. Thus, in such cross-border transactions, even though the discount includes VAT (of another member state), it’s not possible to reduce the VAT payable to the Treasury. And such a discount to the end consumer in another member state need not be reported on the VAT return.

On the one hand, it makes sense that the manufacturer cannot report a reduction in the VAT due on his national VAT return because the discount does not include VAT of the manufacturer’s country. On the other hand, there is unfortunately no mechanism for recovering such VAT in the end consumer’s member state. This has been confirmed by the CJEU.

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question