In early 2024 the State Revenue Service (SRS) published an advance tax ruling issued to a foreign company’s permanent establishment (PE) in Latvia, in which the SRS assessed the PE’s relationship with its foreign head office and explained whether the PE is liable to prepare and submit a transfer pricing (TP) file for their mutual transactions. In this article we outline what the tax ruling says about PE status, examine Latvian TP rules on documenting relationships and TP, and offer a theoretical example to explain the PE’s obligation to document TP in practice.

It follows from the SRS tax ruling that under local and international law the PE:

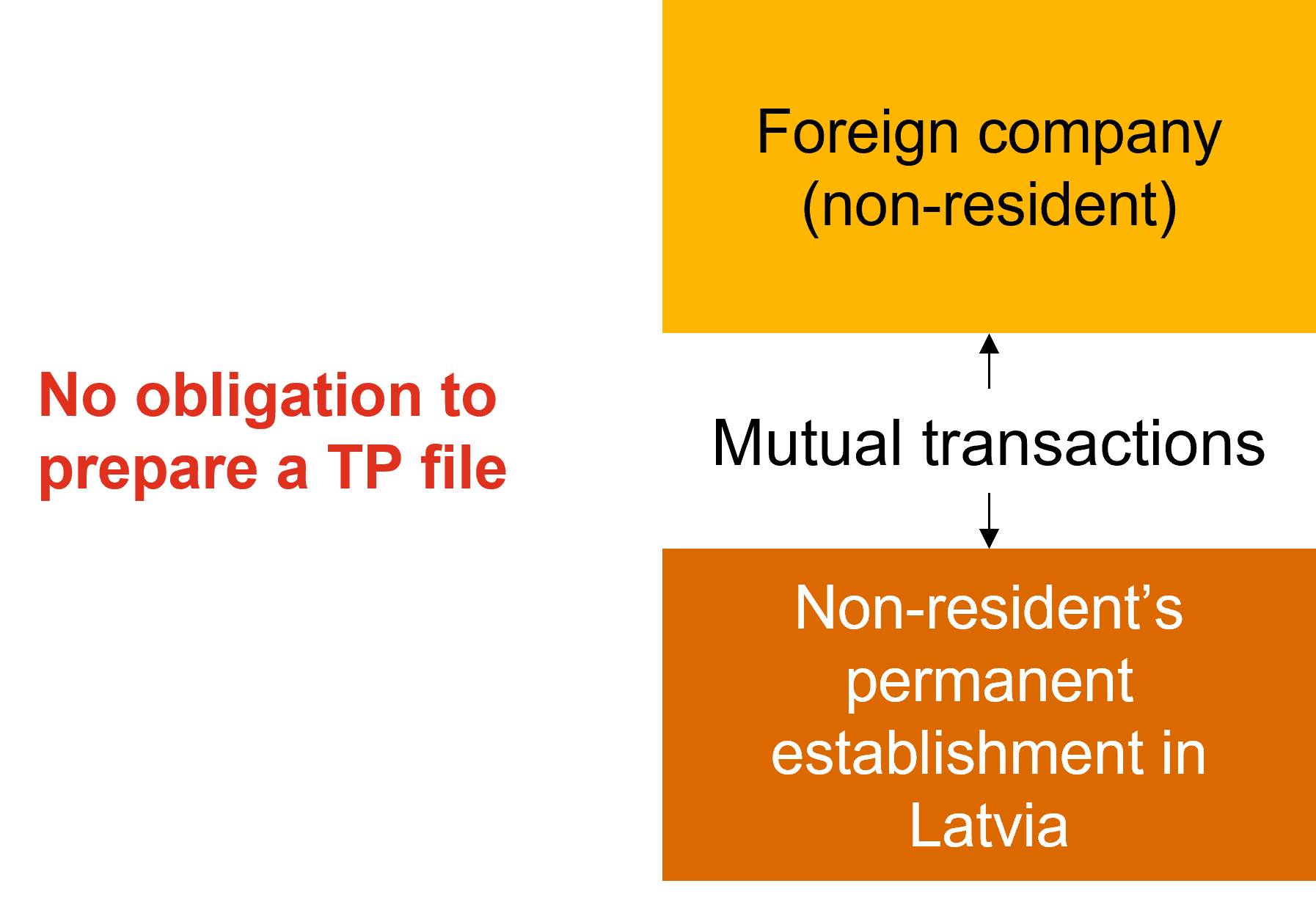

We understand that the PE is the non-resident’s branch in Latvia, not a separate company in its own right. If the PE carries on a systematic business in Latvia, it’s liable to register as a taxpayer with the SRS when starting the business.

The taxpayer’s obligation to prepare and submit a TP file is governed by section 15.2(2) of the Taxes and Duties Act.

The TP requirements for a PE are explained in the SRS tax ruling, which takes a closer look at situations the PE can face.

|

This is not a transaction with a related party |

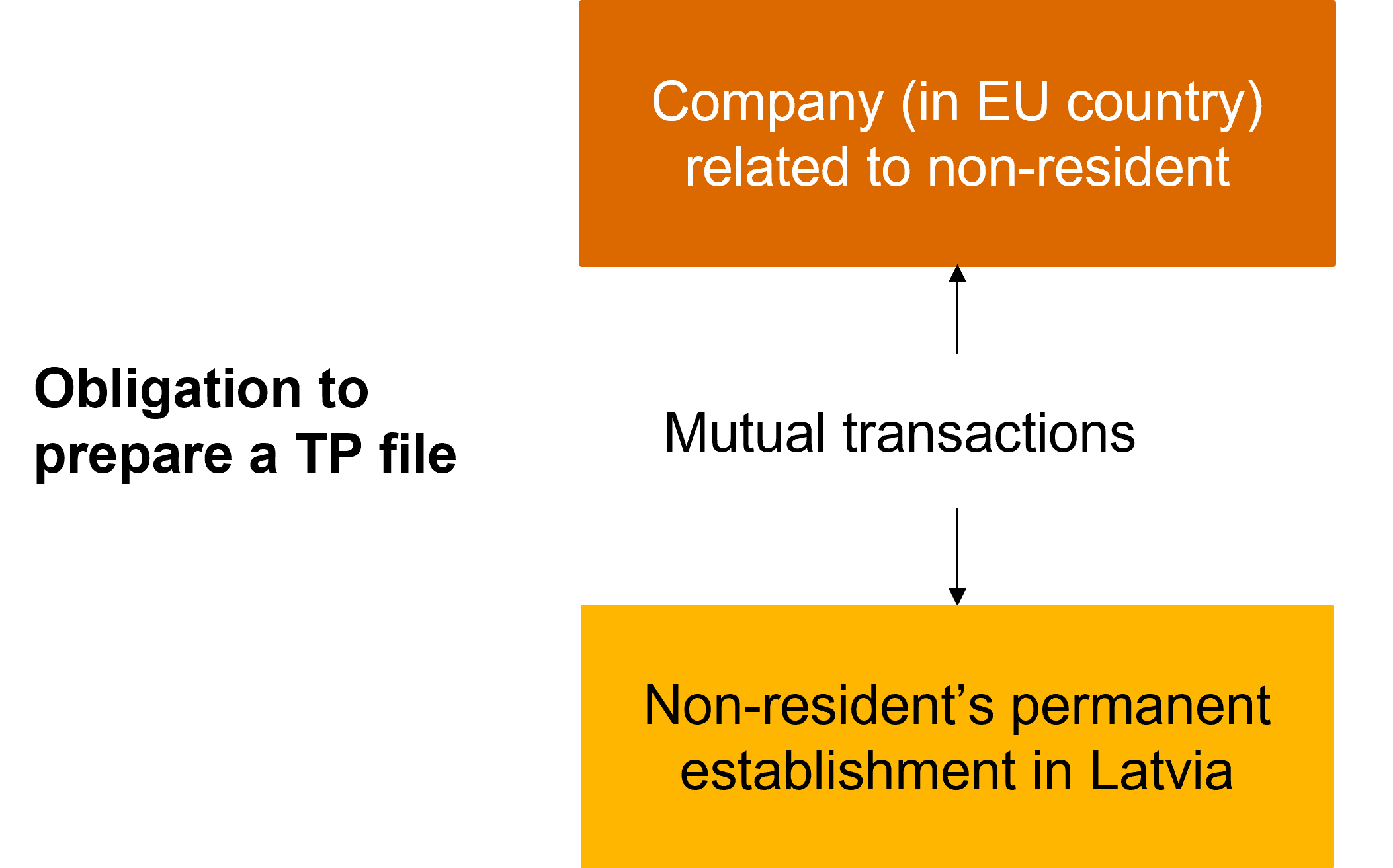

This is a transaction with a related party |

|

According to the SRS tax ruling, the PE’s relationship with the non-resident is not considered a transaction with a related party because it takes place within a single company. |

If the PE makes transactions on the non-resident’s behalf with a person related to the non-resident and that person carries on a business outside Latvia, then these are controlled transactions, meaning the requirements for preparing and submitting a TP file apply to the PE and make it liable to demonstrate that the transactions are arm’s length. |

|

Accordingly, the invoices issued and received between the PE and the non-resident are not controlled transactions, and the PE is not liable to prepare and submit a TP file for its relationship with the non-resident. |

|

|

|

|

A non-resident company buys goods from a related party in the EU and sends some of them to its PE for distribution in Latvia.

All costs associated with the PE’s operations, i.e. the non-resident’s arm’s length acquisition cost as well as any other direct and indirect costs the non-resident incurs, are allocated to the PE.

Since the PE’s relationship with the non-resident is not considered a transaction with a related party because it’s part of the business conducted by a single company, the Latvian PE is not liable under section 15.2(2) of the Taxes and Duties Act to prepare and submit a TP file for transactions the non-resident has allocated to it.

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question