This article summarises the provisions of tax laws and other legislation affecting the calculation of personal income tax (“PIT”), national social insurance (“NSI”) contributions and solidarity tax (“ST”) on wages and salaries in 2022.

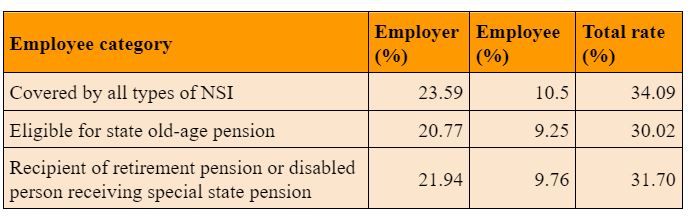

The 2021 rates continue to apply in 2022:

In 2022 the amount of income attracting NSI contributions is capped at EUR 78,100 (up from EUR 62,800 in 2021). Once the cap is exceeded the employer must continue calculating and withholding the employer part and the employee part but those payments will be treated as ST contributions.

In 2022 the ST rate is 25%. Any difference between the ST actually paid (34.09%) and the ST charge (25%) will be recorded as an ST credit and refunded to the employer by 1 September in the following tax year.

From 1 July 2021 there is a minimum NSI payment the employer is required to make for an employee that is paid below the minimum monthly wage of EUR 500. The minimum requirement also applies proportionally to two or more employers if the person has two or more jobs paying below the minimum wage. The National Social Insurance Agency will compute the minimum NSI proportion for each employer separately and post payment details on the Electronic Declaration System. While the minimum NSI payment is the employer’s cost, it is not required to appear on monthly or other reports identifying the amount of NSI.

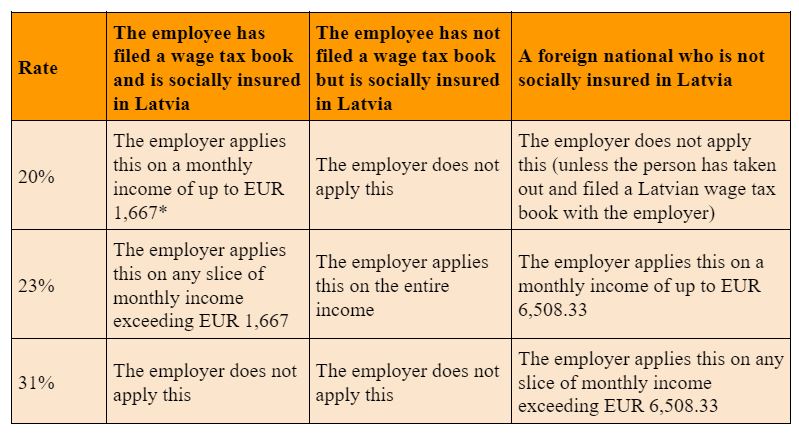

In 2022 PIT applies on employment income at the following progressive rates and thresholds:

* An employee may choose to apply a 23% PIT on their income and refuse to apply the State Revenue Service’s personal allowance forecast for the tax year by making a note in their wage tax book or filing a written request with their employer under sections 15(23) and 30(8) of the PIT Act.

The following items multiplied by 20% are deductible from the PIT charge:

In 2022 the monthly personal allowance cap has been increased to –

(up from EUR 300 in 2021) if the monthly taxable income does not exceed EUR 500. So, in forecasting the income-differentiated allowance, the State Revenue Service will apply a coefficient of 0.26923 in the first six months and 0.38462 in the last six months.

The income-differentiated allowance estimated for each six months will be added up to arrive at the full amount for 2022.

A taxpayer who is simultaneously entitled to extra allowances as a disabled person and as a politically repressed person or as a member of the national resistance movement will receive the higher entitlement.

Wages, salaries and other fees that are paid after 2021 for any employment or other activities carried out before 2022 will attract PIT and allowances at the old rates.

In 2021 significant changes were made to the PIT and NSI treatment of persons working under the royalties scheme. From 1 July 2021 to the end of 2022 the payer of royalties must withhold a 25% or 40% PIT on the entire royalties, without applying a notional expense rate. The PIT withheld and paid to the government will be split between PIT and NSI as 20% and 80% respectively. Unless royalties are paid by a collective management organisation the following PIT rates apply:

From 1 July 2021 and throughout 2022 the payer of royalties is not required to pay a 5% NSI on gross royalties or file the employer’s report with the State Revenue Service. All the payer of royalties has to do is file a statement of amounts paid to the individual under the old procedure and pay tax on or before the 23rd day of the following month.

In 2022 the minimum monthly wage is EUR 500 (as in 2021).

As before, the minimum hourly rate for each month is arrived at by dividing the minimum monthly wage by the normal working hours for the month. For example, if an employee is to work 160 hours a month (40 hours a week) their minimum hourly rate will be calculated as follows:

500 / 160 = EUR 3.125

In 2022 the employer must pay this duty monthly at a rate of EUR 0.36 for each employee that has an employment relationship and for whom seasonal farmhand income tax is not paid.

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question