In the Baltic countries, the format of the transfer pricing (TP) documentation and the scope of the information to be provided therein are largely uniform and in line with the revised TP documentation standard of the Organisation for Economic Co-operation and Development (OECD). However, the thresholds set by Latvia and its neighbouring countries, above which the corporate taxpayer (CTP) is obliged to prepare and submit TP documentation to the tax administration annually or upon request, differ significantly. In addition, different deadlines have been set for the preparation of TP documentation and the liability for non-compliance with the mandatory requirements. The approach to determining the arm’s length price (market value) is also different in each of the Baltic countries.

This article looks at the latest developments in the field.

The obligation to prepare the TP documentation and include certain information is governed by:

It is important for the CTP engaging in international transactions with related parties to know the details of the obligation to prepare and submit TP documentation.

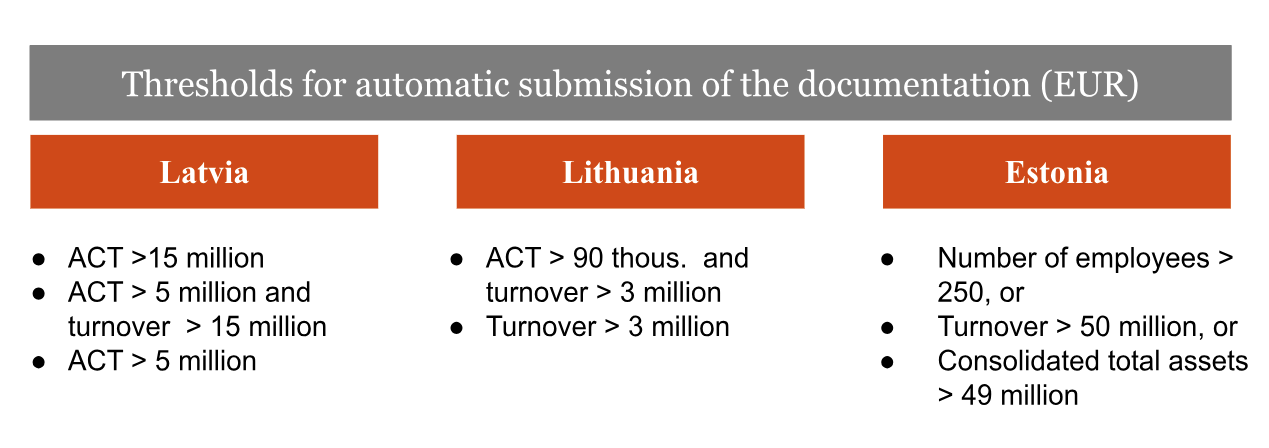

It is important to keep a close eye on the TP legal framework, as the requirements for both certain thresholds (turnover, the price of the controlled transaction (CT), number of employees) and the amount above which the CTP has an obligation to prepare and submit the TP documentation differ significantly in the Baltic countries.

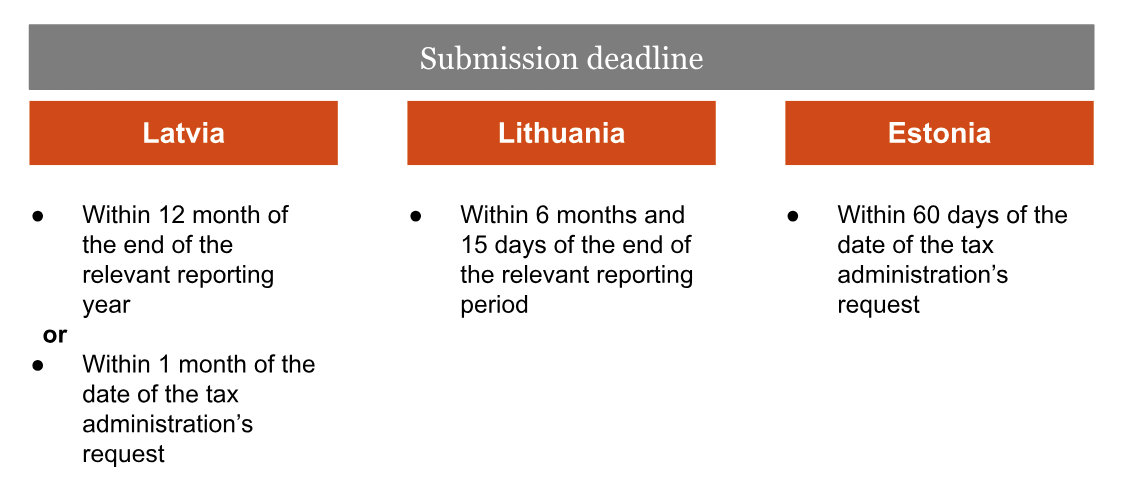

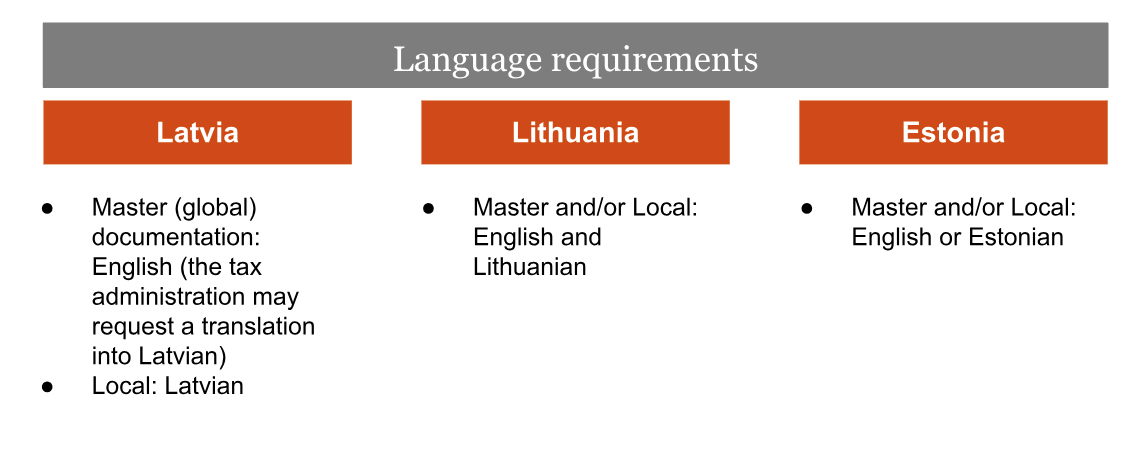

In the tables below, we have compiled information on the requirements of each national legal framework for:

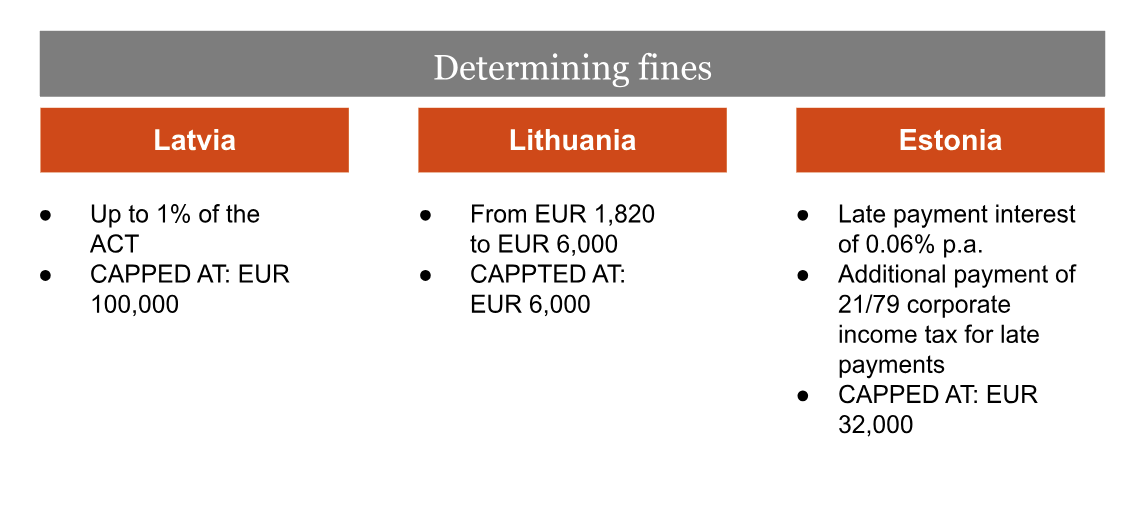

It should be fully accepted that it is important to submit best quality TP documentation in a timely manner so that the tax administration can effectively control the accuracy of tax payments. However, the liability provided for violations of the deadline for submitting TP documentation or the requirements for the preparation thereof is established differently in each of the Baltic countries.

In the table below, we have summarised information on the scope of responsibilities in each country:

In particular, it is worth noting that in September 2023, the Latvian tax administration published guidelines on the principles for imposing fines if the deadline for the submission of TP documentation or the requirements for the preparation thereof is not met, and the criteria for determining their appropriateness.

When determining an arm’s length profit level indicator range, the financial data of comparable independent companies is used.

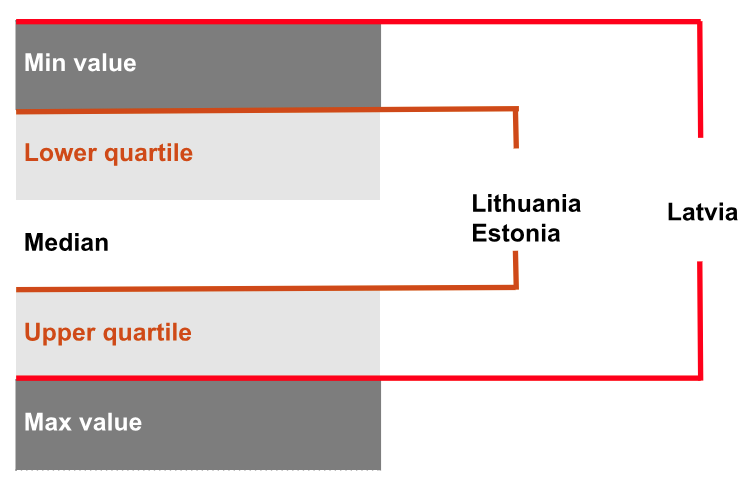

Furthermore, there are also significant differences between the Baltic countries in this process of comparability. To determine the arm’s length transaction/data range, the Latvian TP legal framework allows the use of any established arm’s length price (minimum, maximum, interquartile and decile) appropriate to the chosen comparison profile, in contrast to Lithuania and Estonia, where only the interquartile arm’s length range can be used for comparative analysis.

Despite the identified differences, the overall purpose of preparing transfer pricing documentation is to provide both legal certainty to taxpayers and information to the tax administration as to whether the transfer prices applied in controlled transactions between related parties are consistent with the arm’s length principle.

Please contact us if you need help/advice on the requirements for the preparation and submission of TP documentation in the Baltic countries.

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question