In October 2019, the State Revenue Service (SRS) published an advance tax ruling1 on the corporate income tax (CIT) and personal income tax (PIT) treatment of dividends paid out of profits formed by proceeds from selling a subsidiary. The ruling answers some long-awaited questions about the tax implications.

Background

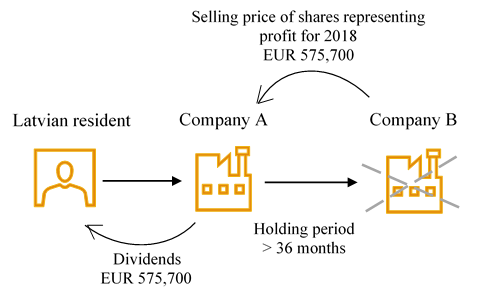

Company A held shares in Company B for more than 36 months. In 2018, Company A sold Company B and received income that represented a profit for 2018 that Company A paid in dividends to its sole shareholder, a Latvian-resident individual, in 2019:

Let us look at the SRS opinion on the CIT implications of Company A’s dividend payment out of profits made in 2018 and on the PIT implications for the recipient of dividends.

CIT treatment

Under section 13(1) of the CIT Act, a company may reduce dividends included in the tax base for a tax period to the extent it received income in the tax year from selling shares held for at least 36 months.

As the initial shareholding period exceeded 36 months, Company A may take relief prescribed by section 13(1) of the CIT Act, i.e. deduct the proceeds from selling shares in Company B from the dividends included in the tax base.

This relief should be taken and disclosed on the CIT return for the month in which dividends were calculated. The company’s tax base from dividends arose in September 2019, so it may take the relief through the CIT return for September 2019.

PIT treatment

As the relief prescribed by section 13(1) of the CIT Act has been applied to the dividends, under paragraph 35.3 of the Cabinet of Ministers’ Regulation No. 899, Applying provisions of the Personal Income Tax Act, the dividends do not qualify for a PIT exemption prescribed by section 9(1)(2.1) of the PIT Act. Accordingly, they attract a 20% PIT under section 15(5) of the PIT Act.

__________________________