Non-fungible tokens (NFTs) have really taken off in recent years. While it might seem this technology has emerged very recently, Kevin MacCoy and Anil Dash created the first known NFT, Quantum, back in 2014. More interest in NFTs didn’t arise until six years later, when the NFT market value reached US$250 million. The market interest in NFTs grew in 2021, when US$41.3 billion was invested in the NFT market over a span of six months. Yet despite such an impressive growth in popularity, we often hear questions like what is NFT, where is it used, and how would it be taxed? This series of articles explores the idea of NFT and the VAT treatment of NFT transactions in the EU.

Judging from the name, an NFT is a digital asset that is unique, irreplaceable, and indivisible. If the NFT is a form of digital art embedded in its software code, then the copyrighted work is the NFT itself.

The NFT may also be merely a digital certificate reflecting ownership of or rights to an indivisible asset – tangible or intangible. In that case the NFT is not the underlying asset but an electronic entry evidencing the right to use the asset. Buying the NFT doesn’t always transfer full ownership of the underlying asset, for instance, its original author retains copyright in the digital work of art. In other words, owning the NFT isn’t always equivalent to owning the underlying asset, unless the NFT agreement provides for the transfer of rights such as copyright.

NFTs are often used in digital art. For example, the creator of a work of art (the copyright owner) gives the NFT owner the right to use the work of art in certain ways under a digital agreement for using the NFT. A typical digital agreement also provides for royalties payable to the copyright holder every time the NFT is sold on, and payment is made using the NFT’s built-in automatic payment function.

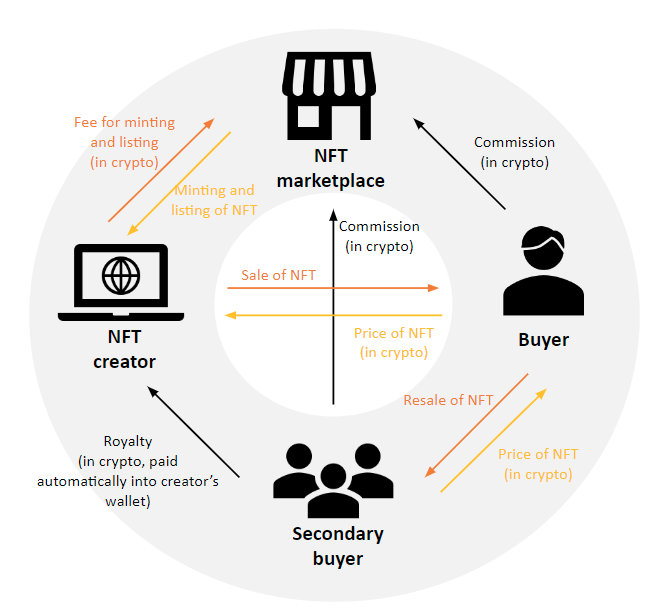

While NFTs are commonly used in selling rights to digital works of art, they have multiple potential uses, such as tangible art, video games, music, and cinema. NFTs can also be used to store and verify information on education diplomas and certificates. This market has attracted various musicians who create their own NFTs, for instance, the Kings of Leon, Eminem, and 3LAU, selling album posters and even music. One of the success stories in the video game industry is CryptoKitties, a game that involves selling NFT cats and has attracted investment of US$12.5 million. Ubisoft, one of the largest video game companies, created Quartz, an NFT that came under a lot of criticism. All these industries have so many examples of how NFTs can be used, suggesting that this market has a great development potential. NFTs can have a variety of business models and they keep evolving. Below is a simple illustration of some current common business models:

The VAT treatment depends on the business model, the terms of a transaction, and in many countries also on how NFTs are accounted for. Most countries have yet to issue laws or guidelines on the VAT treatment of NFTs. The lack of clear rules creates uncertainty about tax treatment.

Spain is among the first EU member states to have published an advance tax ruling on the VAT treatment of an NFT sale between the creator and the buyer. The Spanish tax authority examines the NFT separately from the underlying digital work of art (asset) and evaluates the VAT treatment of the NFT, which is the right to use that asset. The Spanish tax authority finds that the NFT is not a tangible asset and is therefore considered a service under VAT law. In evaluating the type of service, the Spanish tax authority points out that the NFT has the hallmarks of an electronically supplied service, i.e. it is supplied –

It’s important to note that the Spanish tax authority examined only one of possible business models and types of NFT creators’ income. There is no guarantee that other countries will follow the Spanish example in determining the tax treatment of NFTs, but the early signs suggest this. Our next article on NFTs will be exploring how to determine the place of supply of an electronically supplied service and which country should charge VAT on NFT transactions.

For more information on NFTs go to PwC’s report on NFT legal, tax and accounting considerations, PwC’s overview of VAT treatment of NFT in different countries, and PwC’s Annual Global Crypto Tax Report 2021.

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question