A foreign company planning to do business in Latvia can choose between registering a subsidiary or operating through a branch. This choice is commonly dictated by the group’s governance strategy and long-term plans in Latvia. A foreign company going for a simplified arrangement can register either a branch with the Enterprise Registry or a permanent establishment (PE) with the State Revenue Service (SRS) only for paying Latvian corporate income tax (CIT). This article outlines some CIT and accounting issues relevant to PE activities in Latvia.

To pay its CIT liabilities, a foreign company can opt to register a branch with the Enterprise Registry or a PE with the SRS for tax purposes only. Please note that a representative office registered with the Enterprise Registry is not a PE because it is not authorised to trade.

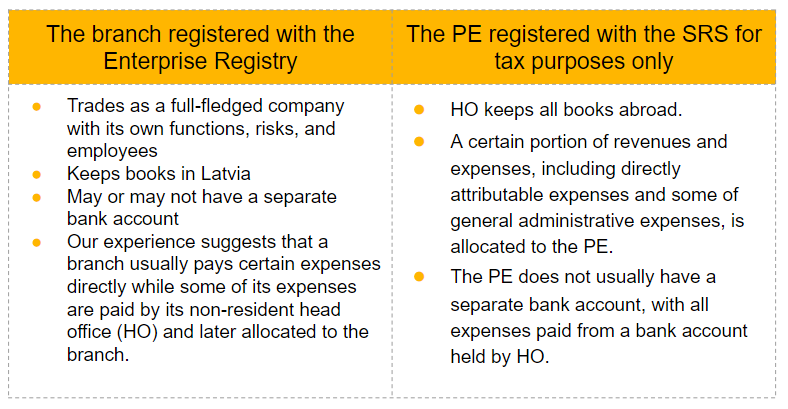

Let us now look at typical characteristics and differences according to the type of registration.

Either scenario offers easy terms for filing financial information with the SRS – the PE does not have to prepare a full set of financial statements. To compute its CIT liability, the PE has to file the balance sheet and the profit and loss account, along with the CIT return.

The PE records its operating revenues and expenses as well as assets and liabilities for CIT purposes separately from HO. No taxable item will arise until the PE distributes profit. The PE pays labour taxes for its staff and VAT under general procedure.

No separate PE bank account

If all customer revenues derived through the Latvian PE are paid directly into the HO bank account, then to establish when HO earns income from the PE and when the PE has taxable income (a dividend equivalent in the amount of profit) that must be reported on the CIT return for the tax period, HO has to ensure the revenues and expenses related to the PE’s activities are recorded separately from HO’s.

Separate books

HO may allocate relevant revenues to the PE once a year, but no later than the last month of the branch’s financial year. The branch will be considered to be making its annual profit distribution.

The PE reserves the right to adjust its taxable items for expenses directly related to its business or for general administrative and day-to-day management expenses capped at 10% of payments the PE has made to HO.

No separate books

If revenues that are derived through the Latvian PE and paid directly into the HO bank account are not recorded in separate PE books, the CIT base for the PE’s tax period must include the entire revenue collected from customers in Latvia during that period (after applying a coefficient of 0.8).

Income extracted from the Latvian PE during the tax period includes:

When it comes to allocating income to the PE, it is important to identify an appropriate profit allocation key, which depends on the scope of the PE’s business in Latvia. We will be writing about this in our upcoming editions of Flash News.

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question