As the tax system evolves, the regulatory authorities have been rearranging their priorities around transfer pricing risks and focusing on increasingly complex cases in recent years. The transfer pricing aspects of intangible assets are climbing up the agenda, so we will be posting a few articles to explain the significance of related-party transactions involving the use of intangibles, as well as looking at transfer pricing trends, common risks, and relevant case law.

An intangible is an asset the company owns or controls that has these characteristics:

It is important to note that intangibles for transfer pricing purposes are not always recorded as such in the company’s books. Costs associated with in-house development of intangibles (e.g. R&D and advertising) are sometimes posted as expenses, rather than being capitalised in the books. So intangibles arising from such expenses do not always appear on the balance sheet. Yet those assets can be used for creating a considerable economic value and should be taken into account for transfer pricing purposes.

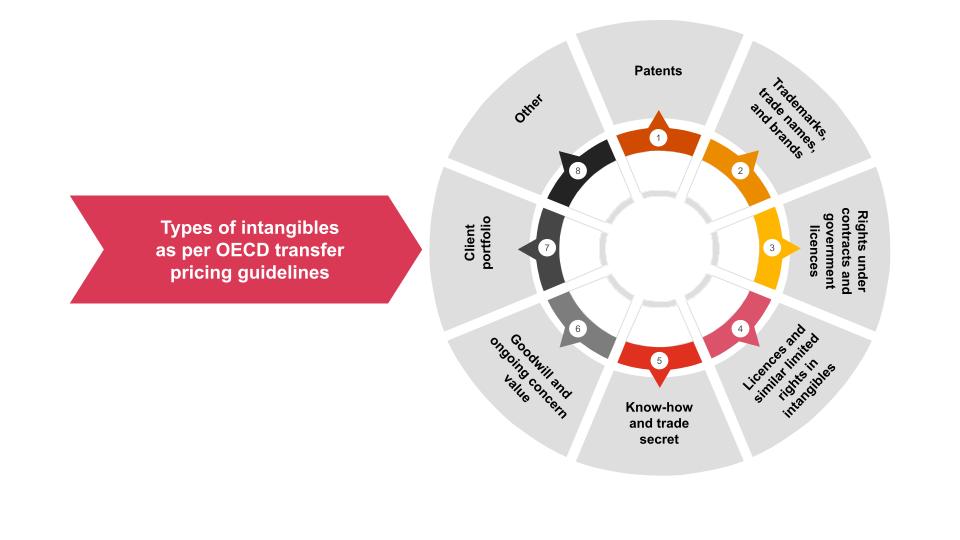

The OECD’s transfer pricing guidelines specify the types of intangibles that are subject to transfer pricing. The picture below shows the main types:

There may be two types of transactions with intangibles once they are split off:

The transfer pricing risks associated with intangibles can be grouped into three main categories:

The main corollary of tax risks associated with intangibles is that licences or other types of payments are used for shifting profits to a jurisdiction with a more generous tax regime or lower rates.

Tax advantages are achieved by having the tax base reduced at the payer’s end by deducting licences or other payments associated with intangibles. The payee, in turn, achieves a tax saving from lower tax rates or a special regime.

In our upcoming articles we will be exploring the concept of “hard-to-value intangibles” and the case law relating to intangibles in general.

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question