For many years, challenging the receipt of intragroup services and commercial benefits has been among the most popular grounds for corporate income tax (CIT) assessments made by the State Revenue Service (SRS). Our analysis of one of the latest publicly available transfer pricing court cases leads to the conclusion that such a taxpayer dispute with the SRS has not lost its relevance. This article looks at an example from the Latvian court case – the taxpayer’s dispute with the SRS over missing evidence that the taxpayer has actually received management services from a related foreign company.

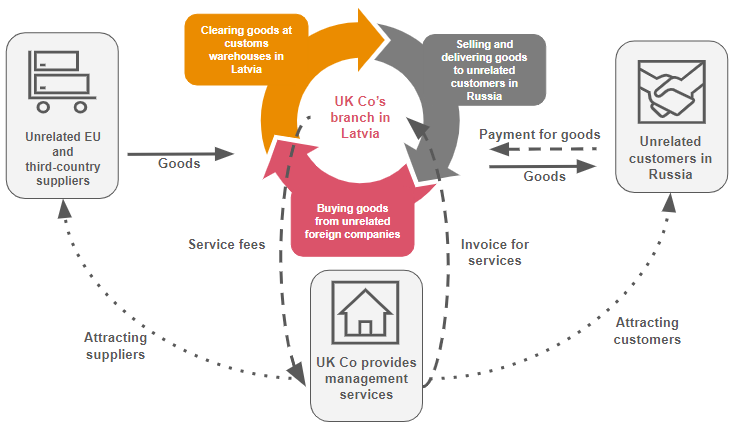

A taxpayer – the Latvian branch of a UK company – purchased goods from unrelated EU and third-country suppliers, cleared the goods at customs warehouses in Latvia, then sold and delivered them to unrelated customers in Russia. According to the taxpayer, looking for suppliers and customers and negotiating terms of business were responsibilities of the UK company’s owner and employee. The taxpayer performed only business support functions. To receive remuneration for attracting suppliers and customers, the UK company invoiced the taxpayer for management services, calculating the fee as a percentage (81–84%) of the taxpayer’s gross profit.

The picture below shows the transaction flows and cash flows:

On 20 December 2021 the Regional Administrative Court heard an administrative case based on the taxpayer’s application to overturn an SRS decision where as a result of an audit the SRS challenged receipt of EUR 10,817,046 worth of management services, assessed CIT of EUR 1,624,202 and a penalty of EUR 487,260.6, reduced a VAT refund by EUR 916.36, and assessed a related penalty of EUR 183.27.

During an audit, the SRS found that the information on the management services appearing on the invoices failed to describe the substance and type of the services and failed to demonstrate that the services had been actually supplied to the taxpayer. The SRS pointed out that the taxpayer did not have a reasonable explanation of what services he was invoiced for and that his email correspondence with head office representatives was not sufficient to establish that the transactions were in fact carried out by the head office.

It is important to note that during the audit the SRS asked the UK tax authority to check the service provider’s business activities and services supplied. The UK tax authority found that the service provider had not opened an account with UK credit institutions and had not filed CIT returns, and the company was not reachable at its registered office.

The SRS also noted that they failed to see why the value of the management services had been set as a percentage of profit, given the methodology for determining an arm’s length price of similar management services.

Having assessed all the circumstances in aggregate, the court found that the taxpayer did not start out having a clear agreement with the UK company on the content of the management services the taxpayer was to supply. The court also found discrepancies in the taxpayer’s explanations for the content of the management services during the audit and litigation. The court points out that although a change of position as such is neither prohibited nor to be treated as unfavourable to the taxpayer, in the context of all the facts, having assessed the content of the management services, this leads to the conclusion that neither the taxpayer nor the UK company had a clear idea about the content of the management services, and they were looking for arguments to explain those services later.

And in the court’s opinion the fact that the UK company’s officer possibly organised the branch’s commercial activities does not reflect in detail the substance and value of the taxpayer’s management services.

Having assessed all the essential evidence in the case, the Regional Administrative Court rejected the application for having the SRS’s decision overturned.

Concerned with the lack of evidence for the receipt of services, this court case once again shows the importance of taking early preventive steps to mitigate the risk of CIT assessment and drawing up documents with coherent content and detailed descriptions of services and strong arguments proving the receipt of services, the benefit derived, and the methodology for calculating the fees. Although it is prima facie difficult to prove the supply of management services, a set of well-prepared invoices, contracts and transfer pricing documents that uniformly explain the facts and circumstances of the transaction matching the statements of the persons involved in the transaction and the facts and circumstances being tested (e.g. the service provider’s capacity) are likely to secure a favourable assessment from the SRS.

And, as it follows from this court case, the fee-setting methodology plays a key role in proving the receipt of services. Management or other intragroup services with fees based on the service provider’s actual costs plus a markup will prove the supply of services if the total costs are clearly defined and can be checked. Yet we have recently seen Latvian taxpayers’ parent companies tending to control their subsidiaries and issuing profit-level invoices adjusting the services or transfer prices as a percentage of revenue or profit, or as the difference between a trader’s normal margin and the Latvian company’s actual profit. Issuing such invoices is generally accepted practice in global transfer pricing that allows group companies taking the largest part of risks or the owners of intangible assets to receive a part of surplus profits, i.e. the profit from the added business value that exceeds normal profit levels, yet such an invoice can pose a significant CIT risk for the Latvian company. To mitigate risks, we need to carefully evaluate the subject matter of the transaction in order to fit the terms and conditions that could be agreed between unrelated parties, then document in detail the analysis carried out, and draw up other supporting documents (i.e. invoices and contracts) accordingly. Such analysis often leads to the conclusion that the subject matter fitting the actual circumstances of the transaction is disclosed or undisclosed agency services, fees for transferring a certain function or risk, or royalties for intangibles (including customer or supplier databases, business contracts etc) and not management services.

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question