In April 2021 the Organisation for Economic Co-operation and Development (“OECD”) published the Third Peer Review Report on Treaty Shopping, which reflects progress in implementing the BEPS Action 6 minimum standard. This standard on preventing the grant of treaty benefits in inappropriate circumstances is one of the four BEPS1 minimum standards that all members of the OECD/G20 Inclusive Framework have committed to implement (over 125 jurisdictions collaborating on the implementation of the BEPS package). This article explores the main findings of the OECD peer review.

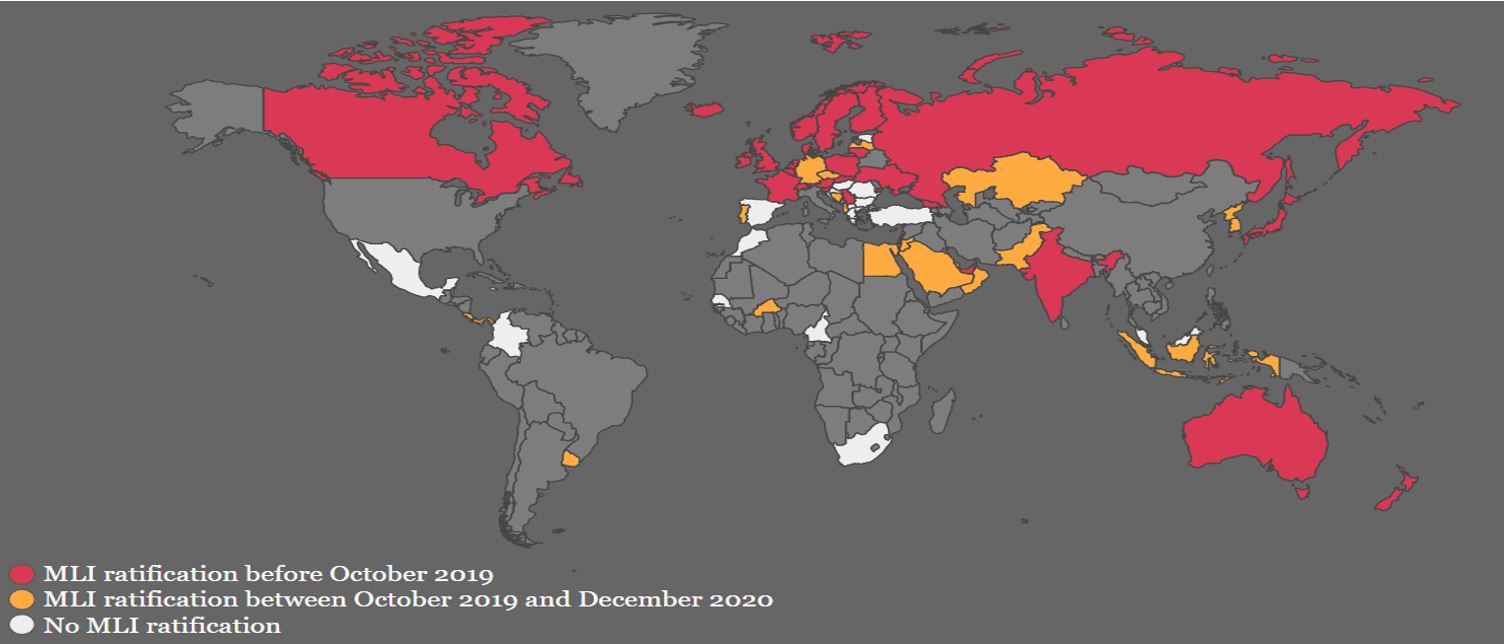

The data compiled for the peer review shows that the Multilateral Convention to Implement Tax Treaty Related Measures to Prevent Base Erosion and Profit Shifting (the multilateral instrument or “MLI”) is used by the vast majority of jurisdictions having started to implement the minimum standard. The MLI is now strengthening the bilateral tax treaty network of jurisdictions that ratified it in 2020. A total of 94 jurisdictions have joined the MLI, 54 have ratified it, and the MLI would, once fully in force, implement the minimum standard in about 1,700 bilateral treaties.

The number of compliant agreements covered by the MLI has increased almost sixfold since 2019 (from 60 to over 350). On average, 30% of the treaty networks of states for which the MLI came into force on 1 January 2020 (Lithuania, Poland, the Netherlands etc) complied with the minimum standard in 2020. By contrast, a mere 1.5% of the treaty networks of states that have not signed or ratified the MLI were generally compliant.

Action 6 of the OECD’s BEPS project has identified the abuse of double tax treaties, in particular treaty shopping, as a major source of BEPS concerns. Treaty shopping typically involves an individual attempting to indirectly take advantage of a tax treaty between two jurisdictions without being tax resident in either. The minimum standard requires jurisdictions to do two things in their tax treaties: make an express statement of non-taxation (normally in the preamble) and use one of three methods to prevent treaty shopping. It does not specify how the two things are to be achieved (e.g. through the MLI or bilaterally). The three methods are as follows:

The PPT permits the tax authorities to refuse treaty benefits (relief or exemption from withholding tax, deduction of expenses etc) if claiming a benefit was one of the main purposes of a transaction. The LOB rule is designed to ensure a company qualifies for treaty benefits only if it is sufficiently linked to (e.g. tax resident in) one of the treaty countries.

By 1 July 2020, a total of 98 jurisdictions within the Inclusive Framework had over 350 bilateral treaties meeting the minimum standard (including the preamble statement and the PPT), 31 of which added a LOB provision to the PPT. Over 1,300 bilateral agreements between members of the Inclusive Framework were expected to become “covered” tax treaties under the MLI after being ratified by both parties and to comply with the minimum standard once their provisions came into force.

Only 17 treaties are the subject of a bilateral amending instrument that is not yet in force, demonstrating the comparative effectiveness of the MLI in implementing the minimum standard.

The MLI will modify only bilateral agreements listed by both parties. There are about 200 unilateral agreements that will not be modified because only one jurisdiction has listed its agreement under the MLI. There are also about 325 “waiting” agreements that will go unmodified because only one of the parties has signed the MLI.

The peer review has revealed that under the multilateral agreement between 11 members of the Caribbean Community (CARICOM), 10 of which have joined the Inclusive Framework, certain income streams such as dividends may escape taxation entirely through unusual features of the treaty, which provides for almost exclusive taxation of all income, gains and profits at source. These features lead to greater economic integration within CARICOM and carry a greater risk of treaty shopping.

The peer review shows the importance of swift ratification of the MLI, as jurisdictions that have not signed the MLI or implemented anti-treaty shopping measures in their agreements have made little or no progress in implementing the minimum standard.

The OECD will carry on monitoring the implementation of the minimum standard, with the next peer review due in the first half of 2021.

Latvia signed the MLI in 2017 and it came into force for Latvia on 1 February 2020 (more details here).

Latvia has 62 effective tax treaties, two of which (with Japan and Switzerland) meet the minimum standard, usually implemented by including the preamble statement and the PPT.

Latvia has not listed its agreement with Germany but has stated that bilateral negotiations are under way. Also, Latvia has not listed its agreement with North Macedonia. The two countries, however, have listed their agreements with Latvia. Under the MLI those are “non-covered” agreements (i.e. treaties between pairs of MLI signatories where one party has not listed the treaty or has not signed the MLI). Listing its agreement with North Macedonia or entering into bilateral renegotiations will help Latvia implement the minimum standard in that non-covered agreement.

__________________________

1 The OECD’s Tax Base Erosion and Profit Shifting project

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question