Directive (EU) 2023/2225 requires businesses to provide fair treatment and transparency in their loan ads and credit agreements, promoting the protection of consumer rights and the efficiency of the single market.

The directive applies to credit agreements under which consumers (individuals for private purposes) borrow money to buy goods and services, namely consumer credit. However, not all agreements that bear the formal hallmarks of a consumer credit agreement will be governed by the directive. The directive provides for several exceptions falling outside its scope, but this does not mean the principles of fair commerce should not be followed in such cases.

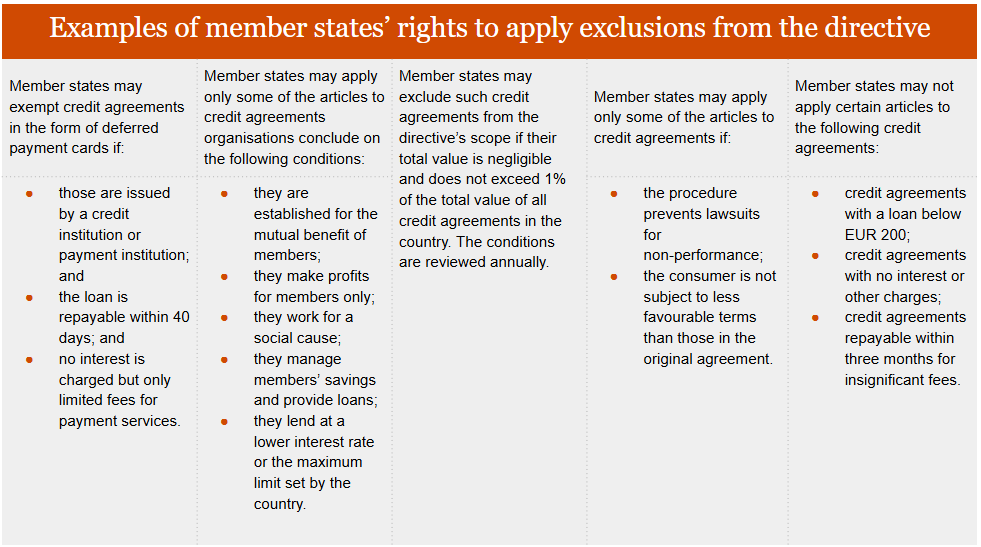

The major1 exclusions are:

In addition to these exclusions, each member state has the right, when transposing this legislation, to impose more or less stringent requirements than those set out in the directive, where this is expressly provided for. For example, certain types of agreements may be subject to exceptions by exempting a particular type of agreement from some of the directive’s requirements, or conversely, all such agreements may be covered by those requirements.

Latvia’s position on these issues will not become clear until it passes the requirements into its national law. This law is in its early drafting stages.

Stringent requirements for consumer credit advertising

The directive requires that all loan ads must be fair and clear and they must not mislead consumers. This means that ads must not contain any information (whether visual or written) that could mislead consumers about the terms of a loan or give a false impression of its advantages.

Ads will also have to include a special warning to make consumers aware of their obligations and associated costs, for example: “Warning! Borrowing money costs money.” Notices that provide essential information and highlight risks have long been a requirement in other sectors, such as the sale of alcohol and tobacco products. Given the high risks of services provided by this sector when credit obligations are assumed recklessly, a business’s minimum due diligence will in future involve a wider range of obligations to inform the public and consumers. Such notices and warnings are especially important where people’s purchasing power and disposable income have objectively decreased as a result of inflation or other circumstances. Also, the demand for such services rises seasonally, for example under the influence of Christmas gift fever.

The directive prohibits misleading ads that could lead consumers to believe a loan will improve their financial situation. This commercial practice is not very widespread, yet various claims may occasionally be found to be misleading when assessed in a broader context.

For example, ads must not state that a loan will increase financial resources, savings or the standard of living if this is not true. Such statements should definitely be avoided to prevent the company from facing administrative penalties for breaches.

The directive will prescribe a set of particulars to be included in ads. As a rule, ads must include standard information that is clear and easy to read. This information must indicate:

Ads must include an illustrative example with different periods to help consumers better understand the terms, choose the most suitable loan, and make an informed decision about which terms would be more advantageous.

When it comes to imposing more stringent requirements, the directive allows the member states to include provisions in their national law that prohibit advertising which:

These restrictions are introduced to ensure fair and clear communication about commercial practices, to prevent consumer deception, and to promote responsible borrowing, rather than to restrict competition to a certain extent. Various solutions and obligations associated with publishing ads are certainly not new to the industry, but it will have to adapt to the required changes. Latvia has strict requirements in place for consumer credit advertising already, yet implementing the directive is expected to impose more controls on the content of ads.

To pursue best practices now and avoid putting yourself in a position where your advertising campaigns need changing, it’s advisable to make sure you meet the new advertising requirements, whether you operate in one member state or across the EU. The directive stipulates that as member states implement various requirements, they must also introduce sanctions for non-compliance with those requirements. While the directive does not specify any amounts, it does mention principles the sanctions should follow.

Bill No. 694/Lp14 has been drafted to amend the Consumer Rights Protection Act and pass the directive’s requirements for consumer credit advertising. The bill is awaiting its second reading.

The range of credits and loans requiring a broader assessment of creditworthiness will expand. When goods or services were acquired on deferred payment terms without interest, not all consumer credit rules had to be followed because such transactions were not classified as consumer credit. Under the directive, such deferred payments are not only restricted in that interest or similar charges may not be applied, but also full payment must be made within 50 days. So, for example, when a computer is purchased on deferred payment terms without interest over a period of two years, this will be considered consumer credit and all consumer credit rules will apply, including a creditworthiness assessment and rules on the content and types of ads. This is a serious step towards promoting responsible credit practices, educating and informing consumers, as well as preventing situations where consumers find themselves in an endless cycle of deferred payments.

Adopting and implementing the directive will expand the framework of obligations for consumer credit providers at the advertising stage. They will be liable to provide extensive information on the terms of obligations and warnings about risks, similar to gambling halls or tobacco purchases, so that consumers taking a loan are aware of possible consequences and understand the full extent of their obligations and payments that will be binding on them. Advertising is often the first step that encourages consumers to borrow, so its content will now be subject to significant controls. Implementing the directive will ensure the consumer receives exhaustive information at the initial stage of lending as well as before entering into an agreement.

It’s also important to await Latvia’s national legislation, which will allow us to understand which of the exceptions left to the member states’ discretion Latvia has chosen to implement.

The directive came into force in 2023, yet the member states still have almost a year to pass it into their national law – this must be done by 20 November 2025. The transposed provisions must become applicable from 20 November 2026. These deadlines are essential for securing a uniform approach to consumer credit across the EU. On the one hand, it can be said there is a sufficiently long period to get ready for applying the new requirements. However, with the general rules on unfair commercial practices in force already, businesses should pay attention to the format and manner in which ads are created and services presented on the market. Consumer credit is currently governed by the Cabinet of Ministers’ Rule No. 691 of 25 October 2016 on consumer credit, and the directive is to be transposed into this rule as well.

The directive also provides for several changes at later stages of consumer lending (e.g. when entering into an agreement). We will explore these developments in our future publications.

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question