ESG or sustainability is a hot topic that people initially associated with the environment and climate change. The social and governance components of ESG have recently become even more relevant when it comes to workers, supply chains or tax management. This article briefly looks at why we should be treating taxes as a key component of sustainability.

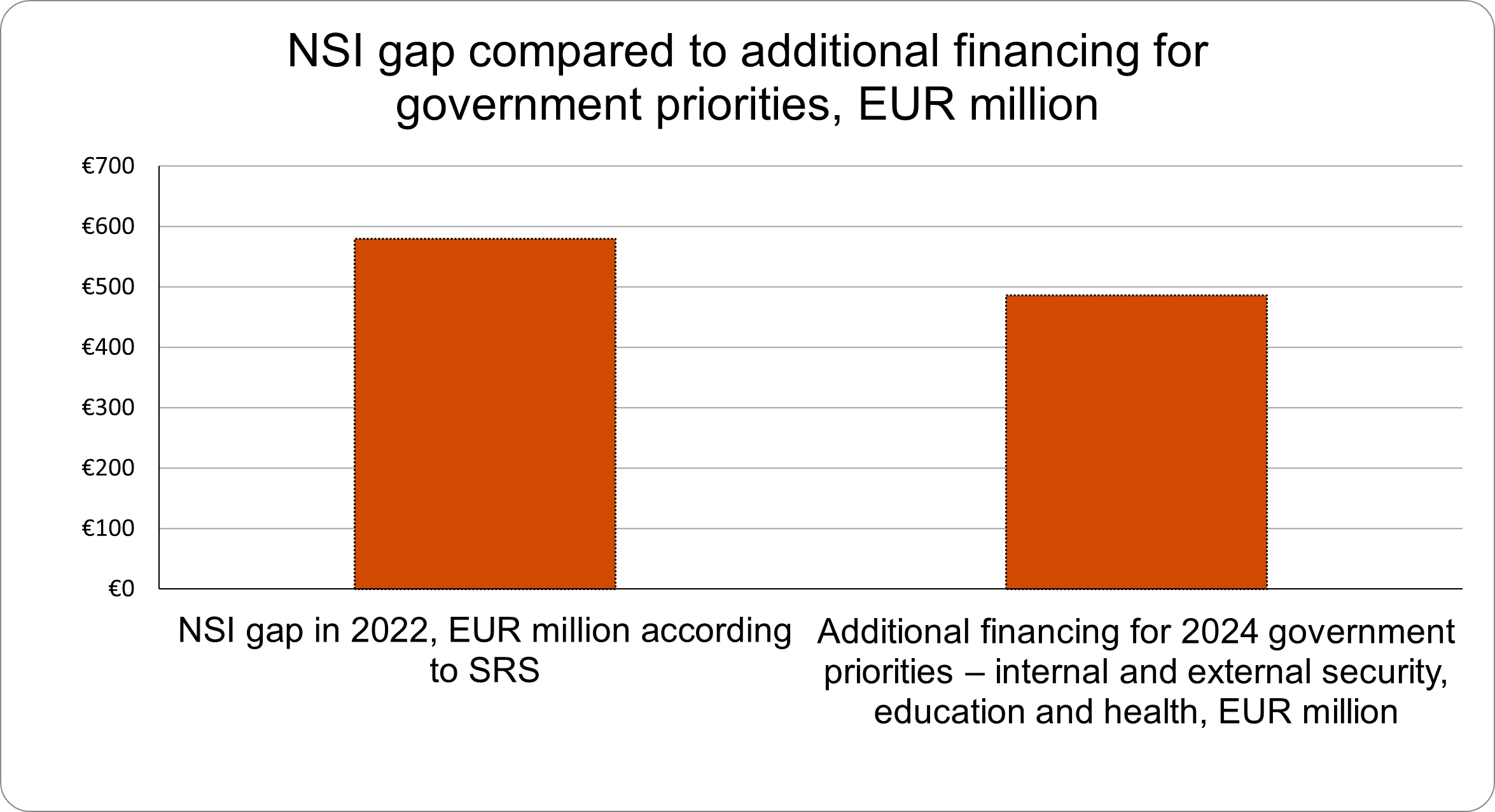

Latvia has 14 taxes, each being charged under a particular tax law. Unpaid taxes, which can be quantified using the tax gap method, for instance, is a part of the shadow economy. The gap for just one tax – national social insurance (NSI) contributions – was EUR 580 million in 2022, according to State Revenue Service (SRS) estimates. For comparison, the extra funding allocated to the 2024 government priorities – internal and external security, education and health (in addition to existing government programmes) – is EUR 486 million. So, if only one of the 14 taxes were duly paid, Latvia would be able to double the extra funding for this year’s priorities.

Tax revenues are used to finance a variety of social, sustainability and any other government priorities. While every taxpayer (organisation and individual) is responsible for paying taxes properly and conscientiously, particular care should be taken by large taxpayers and large companies, including those governed by the EU Corporate Sustainability Reporting Directive (CSRD).

About 50,000 companies, including more than 200 in Latvia, are required by the CSRD to disclose information on material sustainability topics and to prepare a sustainability report according to the European Sustainability Reporting Standards (ESRS).

The ESRS cover sustainability topics across the environmental, social and governance pillars and lay down special disclosure requirements. To identify reportable sustainability topics, companies need to conduct a double materiality assessment. This includes assessing your impact on the environment and society (‘impact materiality’) and assessing how sustainability topics can affect your future operations (‘financial materiality’). Some companies could treat taxes as a material sustainability topic, given the significance of tax contributions to the community and tax compliance scrutiny by investors. Those companies will have to disclose particular information on their approach to paying taxes. So it’s important to consider tax aspects in the double materiality assessment.

If your company has a material sustainability topic that remains unaddressed by the ESRS (it might well be taxes, for instance) you should still disclose information to help the readers understand sustainability-related impacts, risks or opportunities.

In our August ESG newsletter, we will be writing in more detail about how you should disclose tax information in your sustainability report if you recognise taxes as a material sustainability topic (you can sign up for our ESG newsletter here).

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question