To compute the price of a controlled support service transaction, we state the total cost incurred in providing the service then add a markup. But some costs are merely recharged without a markup. This article offers an overview of how service fees are set, focusing on so-called flow-through costs that have no element of profit.

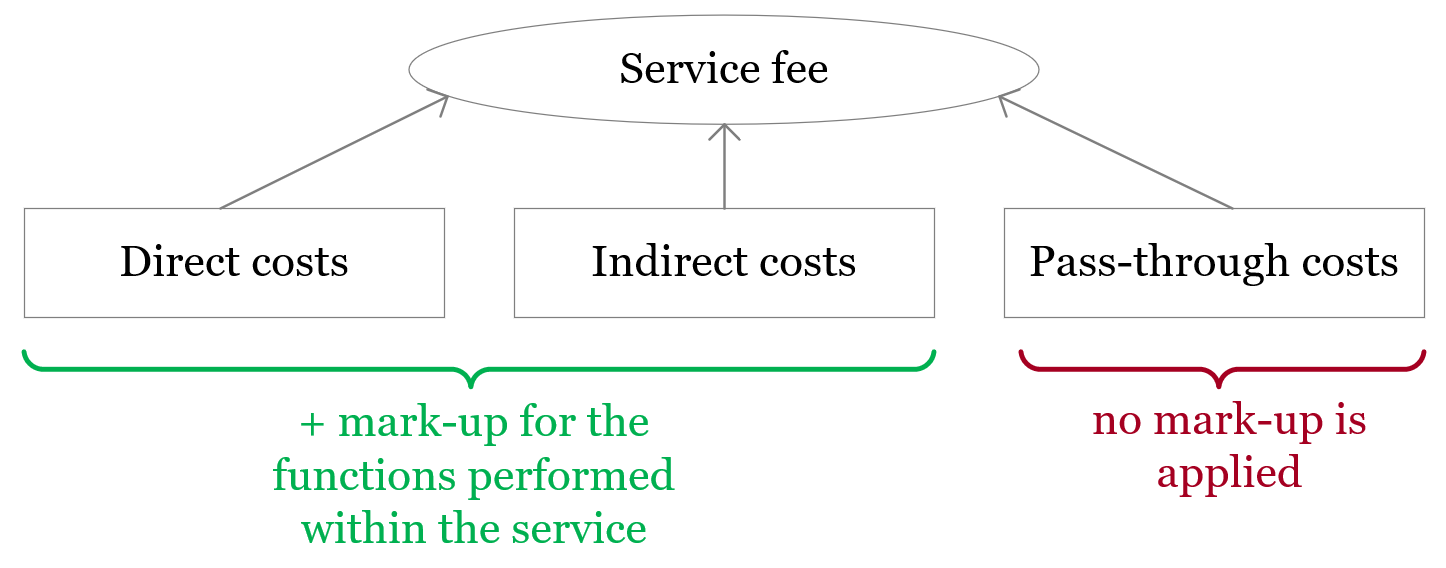

A service fee is made up of all costs incurred in providing it, which may be divided into service costs and function costs, plus a markup. The picture below shows what makes up a service fee:

The following cost categories make up the service fee:

In describing arm’s length fee solutions, the OECD transfer pricing guidelines (starting from the 2010 version) explain1 that the provider of services may pass any third-party costs incurred as part of those services to a related party (the recipient of services) without adding a markup if –

In Latvian transfer pricing rules, “flow-through cost” as a term first appeared in paragraph 18.7 of the Cabinet of Ministers’ Rule No. 677 (effective from 18 July 2019) for low value-adding services, stating that the service provider’s flow-through costs should appear within his total cost and be ignored in computing the value of low value-adding services.

So the taxpayer’s support service costs may include flow-through costs without a markup if he does not change or improve the services acquired from third-party providers and does not take any related substantial risks, but essentially acts as a support mechanism for obtaining those third-party services.

The OECD transfer pricing guidelines offer an example where a related company may incur costs in renting some advertising space on behalf of group members (costs they would have incurred directly if they were independent companies). It might be appropriate to pass those costs to the group recipients without a markup and apply a markup only on costs incurred by the intermediary agent in performing the agency function.

Our experience suggests that a service often involves the service provider organising and paying for services acquired from third-party providers (related and unrelated) on behalf of his related parties. This approach is common practice in groups, with one company performing the function of contracting/purchasing various third-party services necessary for the group companies. This is usually done to achieve efficiencies for the existing intragroup resources (e.g. business agreements with third-party suppliers, and employees with appropriate expertise and experience) and to optimise costs for synergy.

We have dealt with a case where insurance was purchased centrally at group level to cover all the companies under the group’s policy on insurance. The insurance services were actually provided by a third-party brokerage firm that invoiced one group company. This company actually organised the insurance purchase for a fee based on costs incurred in performing this function (salaries for the staff involved, and office and communications costs) plus a markup. The insurance cost is treated as a flow-through cost and recharged to the recipient of services without a markup.

In another case a service provider organised carriage of goods sold to a related company by helping it hire an external carrier. The service provider set his fee by adding a markup to the costs incurred in organising the service, with the third-party transport services being treated as flow-through costs to which no profit element was applied.

To disclose true information on a related-party service transaction and the agreed fee and to assess whether the fee is arm’s length, it is important to provide information on the facts and circumstances of the transaction, state any third-party (flow-through) costs incurred in providing the service, and explain why those costs are ignored in computing the arm’s length fee, i.e. the markup.

_____

1 OECD Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations, paragraph 7.36

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question