Companies in multinational enterprise (MNE) groups increasingly tend to enter into cost contribution arrangements (CCAs) for their joint projects.

The CCA is a contractual agreement between companies to share contributions and risks, which provides that each party will benefit from it. The idea of a CCA is making contributions to achieve a common goal. A core principle of the CCA dictates that each party’s contribution must match its expected benefit.

Taxpayers and tax authorities have developed some international practices and an understanding of how such agreement is regarded from a transfer pricing (TP) and corporate income tax perspective and for other taxes as well.

The CCA is commonly known as “development CCA” under which the parties agree on a common goal: to create and develop intangible property and to apportion intangibles R&D costs and risks in order to become their end users – future beneficiaries.

We have seen in practice, however, that CCAs may also be used for any other joint transaction between group companies to share expenses and risks when there is a common need from which the companies can mutually benefit.

For example, an MNE group may decide to create a pool in order to receive centralised management consulting services, thus combining potential funds to carry on business even more efficiently and to ease the administrative burden by providing and receiving centralised marketing, legal, accounting, IT or other services that don’t create intangibles.

This type of agreement is known as a “service sharing arrangement” whose parties mainly aim to derive present and future benefits from pooling their resources and various skills. The service sharing arrangement is a fairly new MNE practice whose principles confuse taxpayers and tax authorities alike.

This article explores how a service sharing arrangement differs from standard intragroup services, what is known about the corporate income tax treatment of CCAs and TP risks, and what significant benefits a CCA can provide to taxpayers operating in industries that are fully or partially exempt from VAT.

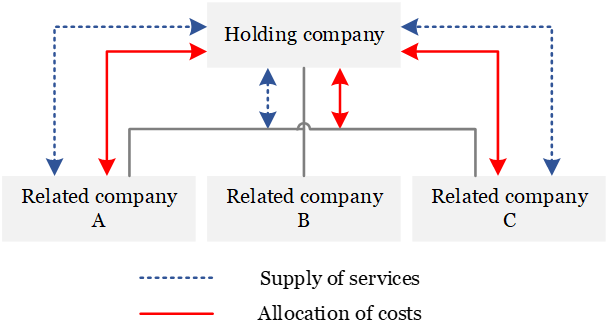

Under a service sharing arrangement, activities are carried out to achieve common goals without providing mutual services. The CCA members identify and estimate functions to be performed according to their expected benefits, i.e. functions are split between the members and they perform each function not only on their own account but also for their partner’s benefit.

Since a service sharing arrangement essentially involves the parties making contributions to achieve a common goal rather than services between related companies, it’s important to state that contributions made under a CCA don’t qualify as services rendered for a consideration. In other words, the parties to a service sharing arrangement cannot have a mutual legal relationship that involves receiving service fees.

The diagram below provides an overview of key features that distinguish a service sharing arrangement from mutual intragroup services, based on the EU Joint Transfer Pricing Forum’s draft report on CCAs and services that don’t create intangibles. It’s important to note that this project was considered when the OECD was drawing up its transfer pricing guidelines.

| Service sharing arrangement | Mutual services | |

|

|

|

| 1. |

There is an agreement on the distribution of risks and rewards under which all the parties make a contribution in cash or in kind (services). |

A service agreement is restricted to services being rendered or acquired by the parties. The risk of services being rendered unsuccessfully or improperly is usually taken by the provider. |

| 2. |

If any of the parties joins or leaves the arrangement, their shares must be balanced according to the arm’s length principle. |

Terminating or renewing the service agreement with one of the parties doesn’t usually affect others. |

| 3. |

A written agreement or other appropriate documentation is important for implementing and performing the arrangement. A written agreement is recommended to enable the tax authority to recognise a service sharing arrangement. The national laws of some OECD countries make a written agreement mandatory. |

In practice, a written agreement isn’t always available. The agreement is often restricted to a direct relationship between the provider and the recipient of services. Yet the provider must be able to show that the service has been rendered, and the recipient must be able to show that the service provides an economic benefit and improves his commercial position. |

| 4. |

Since all the parties contribute to their joint business and their contributions reflect their expected benefits, such contributions are usually measured at their value or cost. |

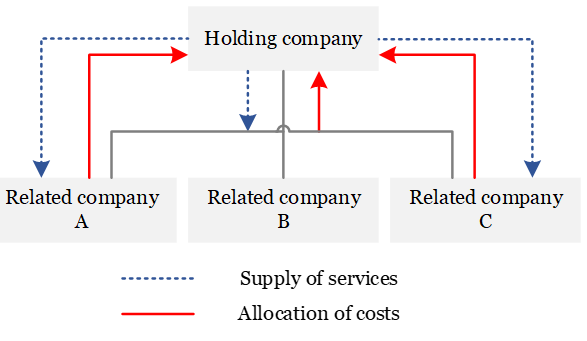

The provider doesn’t use the service for his own needs but rather carries on a business (provides a service) for which he must receive an arm’s length fee to make a profit. |

| 5. |

The apportionment of the contribution is based on each party’s expected benefit. |

The service cost allocation principle is based on the extent to which each company has requested or received, or is entitled to receive, services. |

The main difference between a service sharing arrangement and mutual services is that a traditional provider doesn’t use the service for his own needs but rather carries on a business for which he needs to receive an arm’s length fee in order to make a profit.

While the service sharing arrangement is quite a recent introduction to MNE business, there is some international case law that examines such transactions for compliance and justification. The courts primarily emphasise insufficient evidence of such transactions being consistent with a service sharing arrangement because it’s mostly impossible to show how all the parties benefit from it. This results in transactions between group companies being reclassified as mutual services and leads to a TP adjustment that attracts corporate income tax.

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question