When it comes to performing a transfer pricing (TP) analysis of financial transactions, attention is usually paid to loans and cash pool transactions. Yet there are some other financial transactions between related parties that often fail to receive a proper assessment in the TP documentation: financial guarantees. The current market environment has more creditors such as banks asking for a guarantee before they lend to customers. In this series of articles we explore TP aspects of guarantees, compare different approaches to determining an arm’s length price of a guarantee, and analyse relevant case law.

Companies that are part of a multinational group receive various benefits from the group’s synergy. A key benefit is improved creditworthiness and better terms when borrowing from unrelated parties. Companies in a multinational group usually have a better creditworthiness and may obtain larger loans from third-party banks. It’s important to note that even without an additional guarantee, a group company may get better financing terms as a benefit that is incidental to being part of a multinational group. There are cases, however, where a group company needs financing to expand its business but, despite its stable financial position, creditors refuse to lend the amount requested or are willing to lend at high interest rates reflecting risks associated with the company facing business challenges or a default. In this situation, other group companies may provide a loan guarantee and take the borrower’s credit risk.

For TP purposes, providing a guarantee needs to be analysed as a stand-alone related-party transaction between the borrower and the guarantor that should be priced according to the arm’s length principle. Where the guarantor’s involvement helps the borrower obtain a loan on better terms from a third-party bank, the benefit should be split between the guarantor and the borrower.

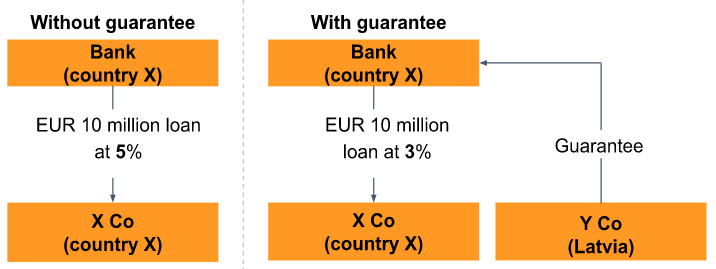

When it comes to analysing guarantees, it’s common to split the benefit into two equal parts. For example, if Company X could receive a loan at 5% without a guarantee and at 3% with a guarantee, the parties’ financial benefit is two percentage points. This means that X will receive a loan at 3% and pay 1% of the loan principal to Company Y for the guarantee.

The figure below shows how the borrower benefits from the guarantee:

This example shows how X benefits from Y’s guarantee. The arm’s length principle dictates that Y must receive a consideration for providing the guarantee to X. The guarantor is subject to additional risk through having legally undertaken to pay in the event of the borrower’s default, which would also harm Y’s financial position.

However, to meet the arm’s length principle, the synergy benefits must be split between the group companies in proportion to their contributions. It’s advisable to split the benefit between the borrower and the guarantor using one of the five approaches described in the OECD’s Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations:

Next time we’ll be looking at each of these methods to determine an arm’s length price of the guarantee.

We invite you to PwC’s Academy webinars "Intragroup services – a potentially expensive transfer pricing risk" on 11 April and "Transfer pricing in loan transactions and their stumbling blocks" on 18 April.

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question