The Organisation for Economic Co-operation and Development (OECD) is known to be a unique forum and a globally recognised centre of expertise that enables member states, including Latvia, to effectively address matters of interest to it regarding the adequacy of transfer prices.

This article looks at the guidance developed by the OECD on Amount B for associated enterprises performing the function of a distributor of goods within a group of companies.

At the beginning of 2024, the OECD published guidelines entitled Pillar one - Amount B. In December 2024, the OECD took the next important step and developed and published tools that are already being used for the practical application of Amount B.

Amount B will be a new approach to arm’s length pricing (value) to justify transfer pricing compliance with “routine” distribution activities for the MNE who perform:

It should be noted that it is difficult to determine the transfer price of the function performed by these companies because it is difficult to find comparable independent companies, mainly due to market consolidation when small independent companies merge or when they are acquired by groups of companies.

Consequently, Amount B will be an excellent alternative to simplifying the compliance of transfer prices for such transactions, since it provides for the setting of a fixed rate of return without carrying out comparative data selections and complex transfer price analyses.

The OECD has developed two tools:

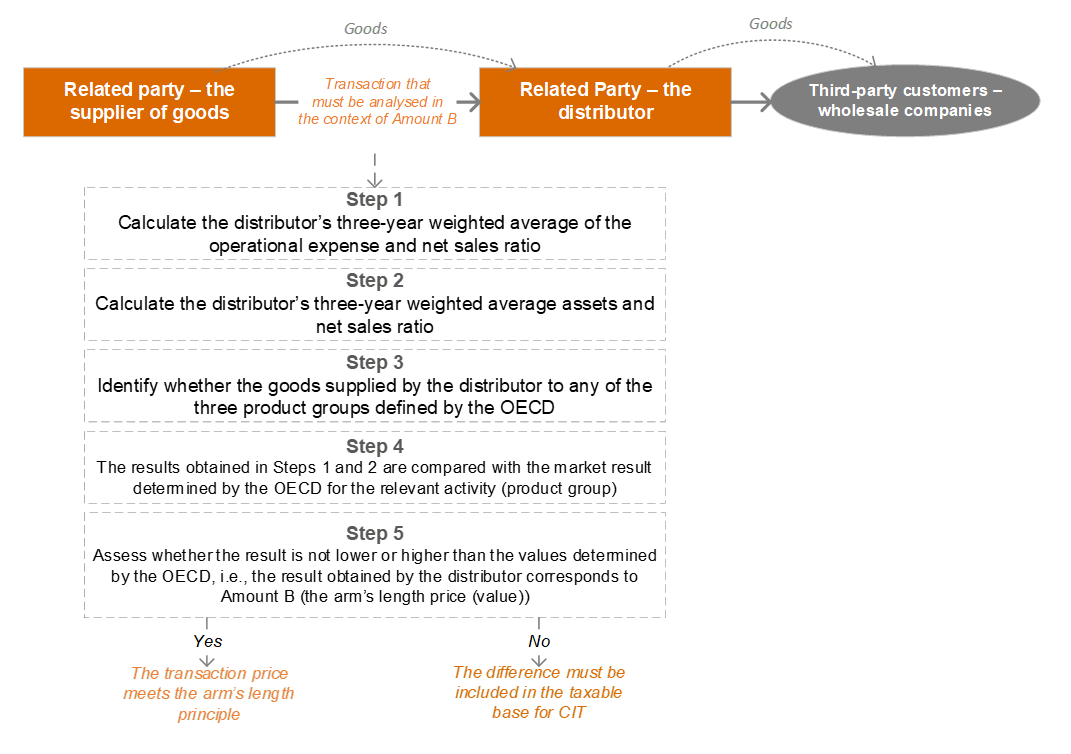

For insight, the structural scheme of the dealer's transaction and determination of the Amount B:

Although the pricing automation tool may seem complicated at first glance, its use requires minimal data entry.

You can familiarise yourself with the tools in detail here.

OECD member states may choose to apply Amount B in their jurisdictions from 1 January 2025 and many member states are looking at incorporating this approach into laws and regulations. At this time, there is no public information on Latvia's approach.

In our view, the use of these tools represents a significant step forward in simplifying global transfer pricing practices. The simplified quantification approach of Amount B will reduce the administrative burden, improve the efficiency and accuracy of determining transfer prices (value) determination and, we believe, help to avoid disputes with tax administrations.

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question