The European Sustainability Reporting Standards (ESRS) require organisations governed by the Corporate Sustainability Reporting Directive to carry out a dual materiality assessment aimed at identifying environmental, social and governance (ESG) areas that are material to them. Unlike the previous practice, which had these areas identified according to the impact made by an organisation, the new methodology adds a further level of analysis assessing the financial impact ESG areas have on the organisation in terms of risks and opportunities. This financial impact can manifest itself, for instance, through the organisation’s:

This means organisations need to ensure their risk management system covers ESG risks affecting or potentially affecting their business in the short, medium and long term. This process has organisations facing a number of challenges mainly associated with scoping the risk and linking it with risks already identified, the choice of assessment methodology, and an objective assessment of risks in the value chain.

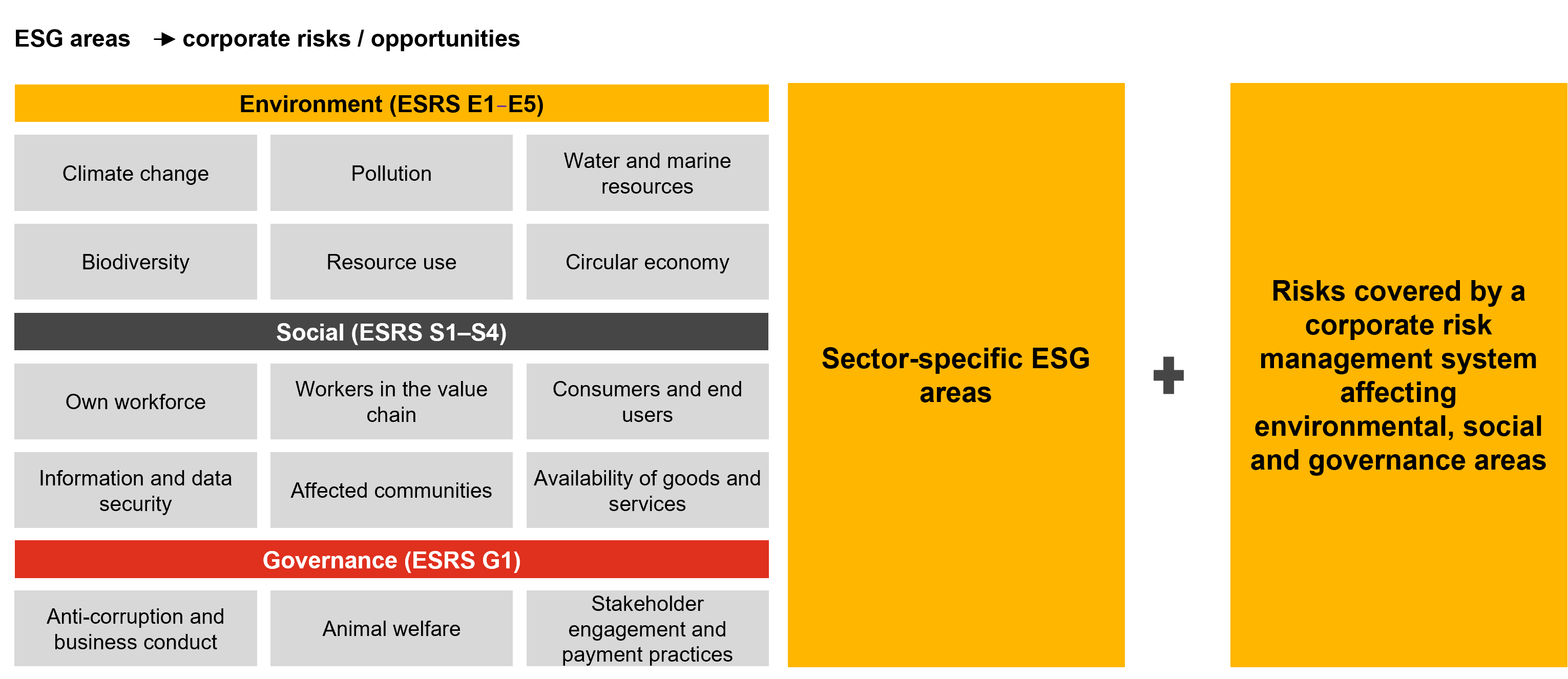

The ESRS require organisations to analyse the areas and topics covered by the impact and financial materiality standards (about 60 different areas) and to identify additional areas specific to the sector an organisation operates in. Analysing this range of areas helps the organisation determine which of them poses or may pose financial risks to its business and add any risks identified by its risk management system to this list.

It’s important to note that ESG risks can materialise in the business of an organisation and in its value chain. So, before identifying risks, it’s essential for the organisation to gather information on key aspects of its value chain, such as where essential links of its supply chain are located and what value they add, as well as their significance in creating its goods or services.

Considering the diversity in terms of scale, sector and other aspects, the ESRS permit organisations to define thresholds for assessing the materiality of identified risks. When it comes to methodology, it’s advisable to use two indicators: the materiality of consequences of an impact and the probability of an impact arising. When assessing the materiality of consequences, we can use considerations such as the availability (physical availability and price) of resources that can be used currently, regulatory changes affecting the impact area, changes in customer habits, and supply chain vulnerability – in the short, medium and long term. Thus, when the total materiality of a particular risk is being assessed, these factors can help estimate the materiality of financial consequences. If the organisation has carried out an assessment of certain ESG risks based on the methodology of its own risk management system, the risk assessment obtained can be transformed to align the dual materiality assessment with the chosen approach.

Certain ESG risks may be difficult to assess, in particular ones that arise in the supply chain. In that case the organisation should use reliable external sources of information such as databases, maps, matrices, indices and assessments at industry and country level. Here are some risk examples:

No matter the approach an organisation takes to assessing ESG risks, this assessment should be based on reliable and objective data sources and expert opinions. As with other operational risks, the organisation needs to identify measures to manage and mitigate ESG risks and include those in its overall risk management system and decision-making process.

This article has been prepared in addition to the new season of PwC ESG Academy’s series of webinars, Module 2, “A practical guide to building sustainability strategies and managing ESG risks”. If you want to learn more about sustainability topics, you can sign up for our webinars via this link.

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question