Passed

While the lawmaker is in the process of revising the Taxes and Duties Act, adding new terminology to describe related parties and their mutual transactions, and contemplating the materiality threshold for a single controlled transaction or a category of controlled transactions that will determine whether related parties will have to file the master file and/or the local file of their transfer pricing (TP) documentation, it is already clear what TP methods taxpayers will be allowed to select for deciding whether the terms of their related-party transactions meet the arm’s length standard. This article explores the TP methods described by the Cabinet of Ministers’ Regulation No. 677 of 14 November 2017, Application of Provisions of the Corporate Income Tax Act (effective from 1 January 2018) as well as their selection and application.

Paragraphs 13–17 of the Cabinet Regulation define methods a taxpayer will be allowed to use in applying the arm’s length principle. There are still five TP methods, of which –

It is important to note that the TP method selection process is always aimed at finding the most appropriate method for a particular case, and the choice of method depends on the facts and circumstances of that case.

Under paragraph 13 of the Cabinet Regulation, this method is applied to transactions involving goods and services with comparable prices.

Under generally accepted principles, this method involves comparing the price applied in a transaction between related parties –

Paragraph 1 of Annex 2 to the Cabinet Regulation offers an example of how the comparable uncontrolled price method is applied.

Under paragraph 14 of the Cabinet Regulation, this method is applied to a reseller’s purchases from a related party if the reseller sells on to an unrelated party.

The price of resale to an unrelated party is reduced by a gross profit out of which the reseller should cover his selling and administration costs to arrive at a suitable margin, considering the functions performed, the associated risks, and the assets used for the conduct of the transaction, as well as other factors affecting its price.

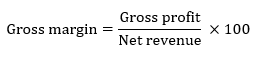

Under generally accepted principles, this method involves comparing the resale price difference (gross margin) a reseller earns in a transaction between related parties –

The resale price difference (gross margin) is calculated as follows:

Paragraph 2 of Annex 2 to the Cabinet Regulation offers an example of how the resale price method is applied.

Under paragraph 15 of the Cabinet Regulation, this method is applied to a seller’s (manufacturer’s) or service provider’s transactions where goods or services are supplied to a related party.

An appropriate markup is added to the supplier’s direct and indirect costs related to the controlled transaction, considering the functions performed, the associated risks, and the assets used for the conduct of the transaction, as well as other factors affecting its price.

Under generally accepted principles, this method involves comparing the markup a seller adds in a transaction between related parties –

The markup is calculated as follows:

Paragraph 3 of Annex 2 to the Cabinet Regulation offers an example of how the cost plus method is applied.

Under paragraph 16 of the Cabinet of Ministers’ Regulation No. 677, this method is applied like the resale price method or the cost plus method where comparing the gross margin of a controlled transaction or the markup on its direct and indirect costs with relevant financial indicators of unrelated parties fails to produce a sufficiently credible result based on factors affecting the transfer price.

Under generally accepted principles, this method involves comparing the net profit a taxpayer earns in a controlled transaction –

Where goods or services are acquired from a related party, the net margin is calculated as follows:

Where goods or services are supplied to a related party, the net profit markup is calculated as follows:

Paragraph 4 of Annex 2 to the Cabinet Regulation illustrates how the transactional net margin method is applied.

Under paragraph 17 of the Cabinet Regulation, this method is applied to interdependent transactions where it is not possible to find comparable transactions between unrelated parties, or to transactions involving multiple related parties.

Under generally accepted principles, this method involves first measuring the combined profit resulting from related-party transactions and then splitting it in an economically sound manner between the related parties according to each party’s contribution to the newly created value.

Paragraph 5 of Annex 2 to the Cabinet Regulation illustrates how the profit split method is applied.

Under the Cabinet Regulation, the right method for determining the arm’s length price of a transaction is selected according to the following factors:

It is important to remember that –

When determining the period for gathering information about a comparable uncontrolled transaction, we can choose –

Applying these methods to transactions involves conducting a comparability analysis (paragraphs 11–12), in which the results of the functional analysis and the following comparability factors are considered:

Comparability analysis involves drawing up a list of key economic activities (functions) and identifying relevant risks based on the functions performed. Those risks should then be compared with comparable uncontrolled transactions or a comparable unrelated party. If material differences are found between the controlled transaction and the transactions or entities being compared, then mathematical calculations or reasonably accurate financial data adjustments can be made to avoid a significant effect on comparability.

We encourage you to consider these references to the new provisions of law coming into force in 2018, and we hope they will inform your company’s commercial judgement about applying the arm’s length principle and using transfer pricing analysis.

If you have any comments on this article please email them to lv_mindlink@pwc.com

Ask question